Position Sizing Explained

Many Forex traders, if not most, trade a fixed number of contracts every time and trade the same number of contracts in each of the currency pairs they trade. It can be conclusively demonstrated statistically that trading the same fixed number of contracts in every trade is not the best methodology and that varying the number of contracts over time and among currencies is far better.

Position sizing is a money management tactic to ramp up profitability by adjusting the number of contracts you trade. Position sizing is different from changing the number of contracts progressively as a trade moves in your favor, named scaling in.

Position sizing dictates the number of contracts you trade before you take the trade, unlike scaling in. There are two ways of applying the position sizing concept. The first is to go from a fixed position size, say one or two contracts per trade, to a percentage risk basis, also named the fixed fractional method, meaning a specific maximum loss per trade as a percentage of capital (such as the classic 2%). You determine how many contracts to trade based on the proportion of capital you are prepared to lose, which is a function of your stop-loss. A variation of the percentage risk/fixed fractional method is named the variable fractional, meaning you alter the percentage at risk based on factors external to the trade, such as the strength of an indicator/breakout or some other reason to raise or lower the percentage of capital you are willing to lose. These methods are presented in detail in the next lesson.

Another important application of position sizing is to alter the number of lots you are trading among currency pairs. Instead of trading one lot per currency pair per set of trades, for example, you would do three lots in one currency pair, two lots in another, and one lot in a third. You allocate a different number of lots according to recent profitability, increasing the number of contracts you are trading when gains in that currency pair are generating high profits and no or low losses. It does not matter whether the gains are due to your excellent trading system, or personal astuteness and skill, or any other reason — the point is that if you are making 18% per month in currency pair A and 6% in currency pair B, you should allocate three times as much capital to currency pair A, or triple the number of contracts.

Periodically (such as monthly), you should analyze the gain/loss ratio per currency pair and allocate your capital in upcoming trades according to the recent performance. It is helpful if you understand why currency pair A did better, but it is not necessary. In some cases, allocating the next month’s capital in proportion to last month’s gain/losses can yield more enhancement of return on capital than any other tactic, including altering your trading system and style.

The benefits of position sizing in commodities trading were first described in detail by Ralph Vince in his books, including The Mathematics of Money Management and Portfolio Management Formulas. Vince’s books are not for the faint of heart. One of the issues is that Vince recommends basing allocations on a starting point named optimal f, which incorporates the worst loss ever taken in the security. Every other calculation depends on that worst-case loss. This is mathematically sound but very hard to apply consistently going forward when you know perfectly well that the conditions that produced that biggest loss have changed. You also know or should suspect that the biggest loss has not yet been taken.

However, the virtue of Vince’s approach is that you start seeing success in trading as a statistical undertaking. Never mind your Ph.D. in international economics or any other qualification you may have to trade Forex — if you do not get the allocation right, and the allocation begins with worst-case losses — you will have a less-than-optimum P&L at the end. This does not mean you need to learn statistics before you can trade, but it does mean that trading shares some hard rules of the road with gambling. As you may know, a great deal of early statistical work started with the study of gambling.

Vince’s optimal f is actually a refinement of the most famous allocation system devised for gambling, the Kelly criterion, named for the mathematician who (in 1956) devised the methodology that was ultimately used by many others as far afield as casino gambling and Wall Street, including, it is rumored, by Warren Buffett. The most famous follow-up book to the Kelly journal article is Beat the Dealer by Edward Thorpe (1956). The most comprehensive (and readable) review is Fortune’s Formula by William Poundstone (2005). If you read one book on the mathematics of trading, Fortune’s Formula is the one to get.

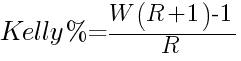

The math behind the Kelly criterion is heavy going for most readers, but here is the essential point: the percentage of your capital that you should place on your trade (the bet) is equal to your edge divided by the odds. Your “edge” is the probability that your trade will be a winner, and you know that probability from your historical trading results. The odds are your gain/loss ratio.

where:

— the percentage of capital to be put into a single trade

— the percentage of capital to be put into a single trade — winning percentage of a trading system over time

— winning percentage of a trading system over time — average gain/loss ratio over time

— average gain/loss ratio over time

Using the Kelly %, you will get “optimal” growth in your capital stake. One issue is that you have to re-calculate it after every trade. Another is that a full Kelly allocation can result in catastrophic losses, something Vince addressed by substituting the worst-case loss in place of the average loss in Kelly’s formula. Some traders try to reduce the risk of the Kelly methodology by doing half the Kelly %, named the “half Kelly” or 25% of the recommended amount, named the “quarter Kelly.”

In 2013, Van Tharp produced a book titled The Definitive Guide to Position Sizing, in which the author modifies the Kelly principles to make them more accessible and easy to apply, if still not intuitively obvious. Tharp asserts that after a strict use of stops, position sizing is the single more powerful force for keeping an account alive. Failure to use stops properly may be the first cause of account failure, but bad position sizing comes next. Some adherents to Tharp's ideas go so far as to say that stop placement is risk management and position sizing is money management, an assertion many others would quarrel with, but the more important point is that you can have the best stops ever designed and if you have lousy position sizing, you will not do as well as you could, even if you do not fail.

Tharp uses what he calls an R multiple, where R stands for risk, but you can understand the reasoning without delving too deeply. As an example, pretend you have $100,000, and you are willing to risk 1% or $1,000 on the next trade. The price of your currency, the AUD/USD, is 0.8950, and your stop is 20 points or 0.8930. Your risk is 30 points or roughly $300.

You divide your predetermined risk ($1,000) by $300 and discover you can buy 3.3 contracts, which we round down to 3 contracts. “Risk” is always the amount of money you are willing to lose in any single trade. In this case, 1R is $1,000. Note that the risk is not inherent in the security’s price movement — it is something you yourself determine. The R methodology does not tell you anything about your profit target or expectation of gain — it simply controls the loss in dollar and percentage terms by trading the right number of contracts. You get to choose your profit target, say 2R or some other number, based on your exit rules. If you manage to exit with a gain of 2R, it would be $2,000 in this case, or 200 points divided by the three contracts or 67 points per trade. Over a long series of trades, having higher gains in terms of R and lower losses in terms of R should be more favorable.

Note that Tharp’s books and seminars are very expensive. Also, note that you do not really have to master the statistics or start running fancy spreadsheets. The key point is to understand that a sane assessment of risk in Forex results in a surprisingly low position size and implies that many traders are taking too much risk by trading a higher number of contracts (as many as the broker’s leverage rules will allow).

EarnForex features two position size calculators you can use in trading: first, a simple web-based form; second, a feature-rich downloadable expert advisor for MetaTrader. Both are free and both will help you to trade the optimal volumes based on your risk tolerance.