Date: 23rd January 2024.

Economic Indicators & Central Banks:

Market Trends:

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Recap: Asia stocks higher; Yen up post Ueda’s comments.

Economic Indicators & Central Banks:

- China: Reports that Chinese officials are looking into a rescue package for the beleaguered stock market has given Asian equities, and particularly the Hang Seng, a big lift. Sources suggest authorities are proposing some $278 bln be invested in onshore funds.

- Japan: The BoJ left policy unchanged, maintaining its -0.100% policy rate and keeping YCC intact, as well expected. BoJ governor Ueda said there is more certainty in the outlook, which saw JGBs paring earlier gains. There were no significant indications on forward guidance. We see more of a dovish lean from the downwards forecasts, with the Bank likely to leave its stance in ultra-accommodative mode until April when the wage talks should be under our belt.

Market Trends:

- Asian stock markets mostly moved higher, with the Hang Seng surging 3% to a session peak of 15,472 before paring gains to 15,345. The CSI rose to 3240 after slumping to a 5 year low of 3218 yesterday. It was at a 2023 peak of 4201 in late January 2023.

- The JPN225 (Nikkei) is up 0.29% to 36,630.

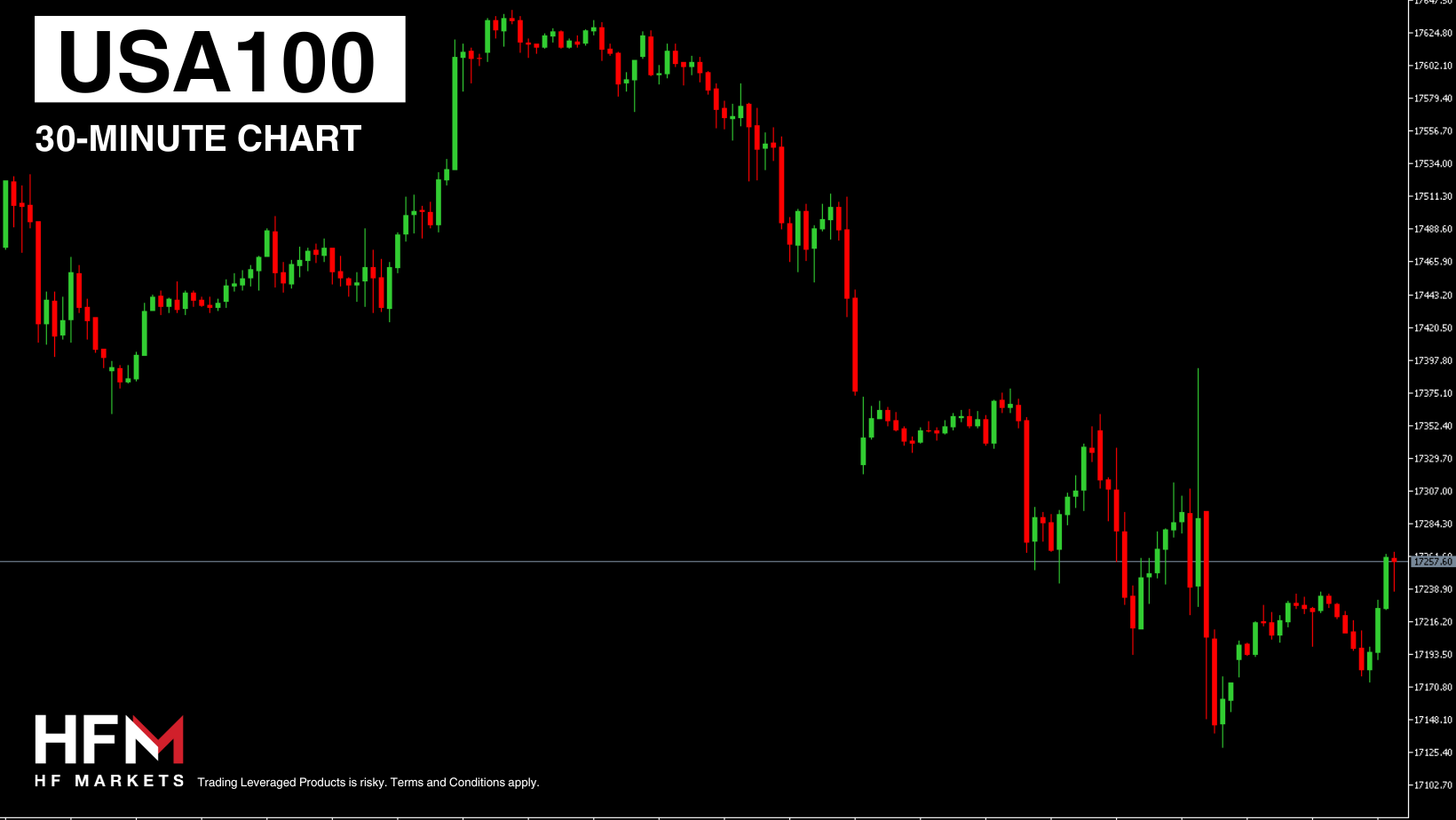

- Stock futures are higher across Europe, but while the US100(NASDAQ) has found buyers, the US30(Dow Jones) is slightly lower but holds above its record high at 38k.

- Microsoft and other tech giants along with Goldman shares, which jumped 1%, have boosted the Dow higher.

- The USDIndex slipped to 102.70 from 103.384 and is seeing broadbased declines.

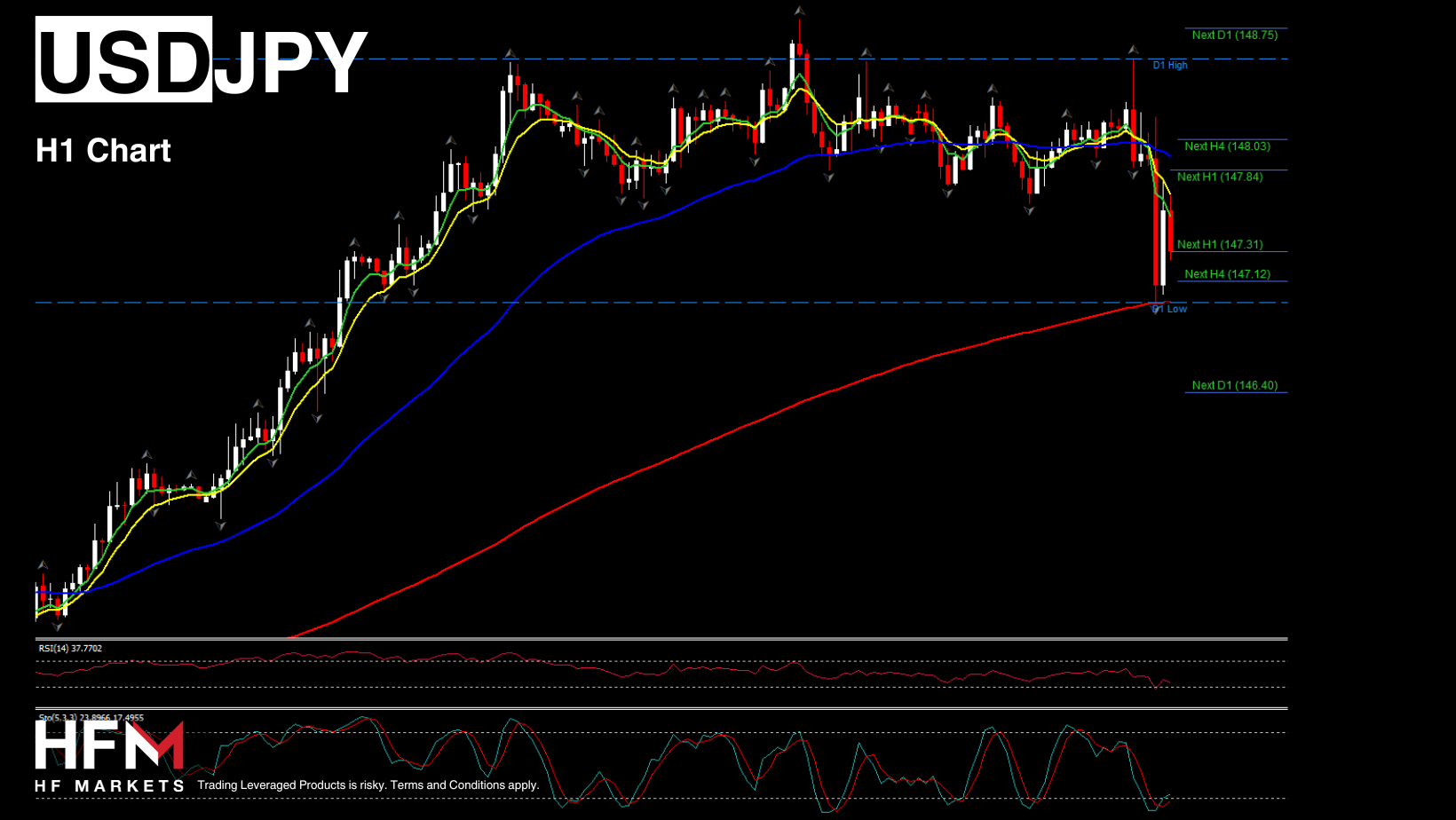

- USDJPY has been choppy, spiking to 148.55 before drifting down to 147.86.

- Oil prices reached $75 again, as US and UK launch new strikes at Iran-backed Houthi rebels in Yemen, adding to the tension in Middle East.

- BTCUSD dropped below $40,000 as the launch of the first US ETF holds the digital currency abated, as investors take profits off the table. Ether, the second-largest cryptocurrency, fell 6% to $2,325.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.