Date : 22nd June 2022.

Market Update – June 22 – Stocks rally, USD & Yields hold, Oil & Yen sink.

USD holds at highs (USDIndex 104.51), Stocks closed up over 2% (NASDAQ +2.51%) – (1) dead cat bounce & another bear market rally or (2) signs of peak inflation and peak Fed bearishness ? (Technicals & Fundamentals still say 1). Asian shares closed lower on rapid spread of new Omicron (Hang Seng -1.49%) Yields rheld their gains. Oil also slumped (Brent -3.42%) Gold & BTC slide sideways. Biden expected to announce temp. tax reprieve on gasoline, BOJ Mins confirmed they will ease further if necessary “without hesitation” USDJPY hits new 24-year high. NZD hit by weak trade data.

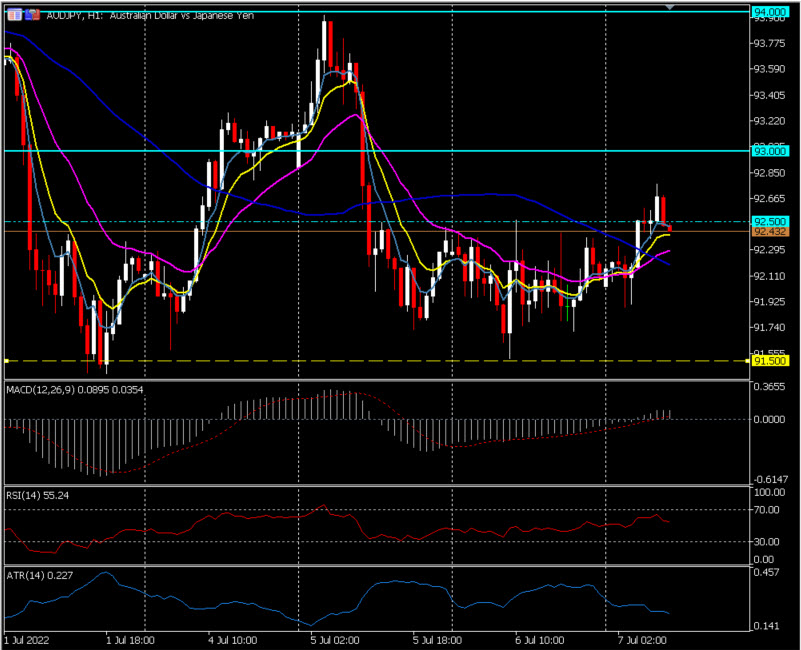

Biggest FX Mover @ (06:30 GMT) NZDUSD (-1.18%). Collapsed from test of 0.6360 on Monday & Tuesday to 0.6250, as NZD Trade Balance missed significantly. MAs aligning lower, MACD histogram negative turning lower, RSI 21.25, OS but still falling, H1 ATR 0.00124, Daily ATR 0.00850.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Stuart Cowell

Head Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – June 22 – Stocks rally, USD & Yields hold, Oil & Yen sink.

USD holds at highs (USDIndex 104.51), Stocks closed up over 2% (NASDAQ +2.51%) – (1) dead cat bounce & another bear market rally or (2) signs of peak inflation and peak Fed bearishness ? (Technicals & Fundamentals still say 1). Asian shares closed lower on rapid spread of new Omicron (Hang Seng -1.49%) Yields rheld their gains. Oil also slumped (Brent -3.42%) Gold & BTC slide sideways. Biden expected to announce temp. tax reprieve on gasoline, BOJ Mins confirmed they will ease further if necessary “without hesitation” USDJPY hits new 24-year high. NZD hit by weak trade data.

- USDIndex tested 103.72 on Tuesday before rallying to 104.55 now.

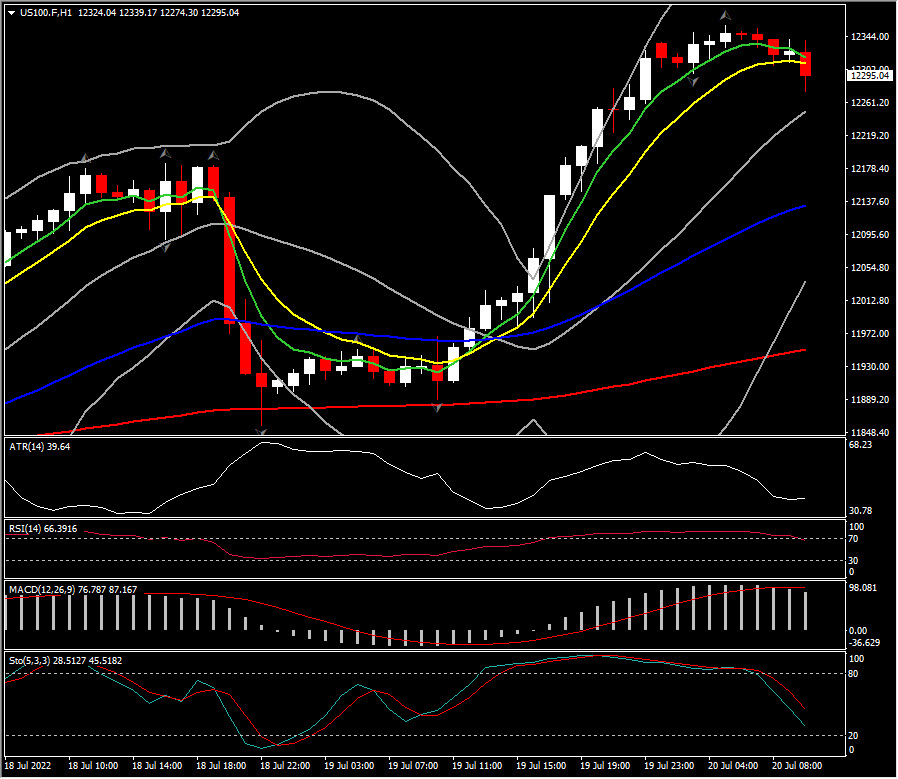

- Equities – USA500 closed +2.45% (3764), US500FUTS slumped to 3719 now.

- Yields 10-year yield higher, closed at 3.26% , trades at 3.29% now.

- Oil & Gold had mixed sessions – USOil slumped 3% to trade at $104.90. Biden & Omicron news weighed & Gold could not hold $1830 and trades at $1825 now on higher Yields and stronger USD.

- Bitcoin continues to pivot around $20K, test $22K yesterday, back to $20K now.

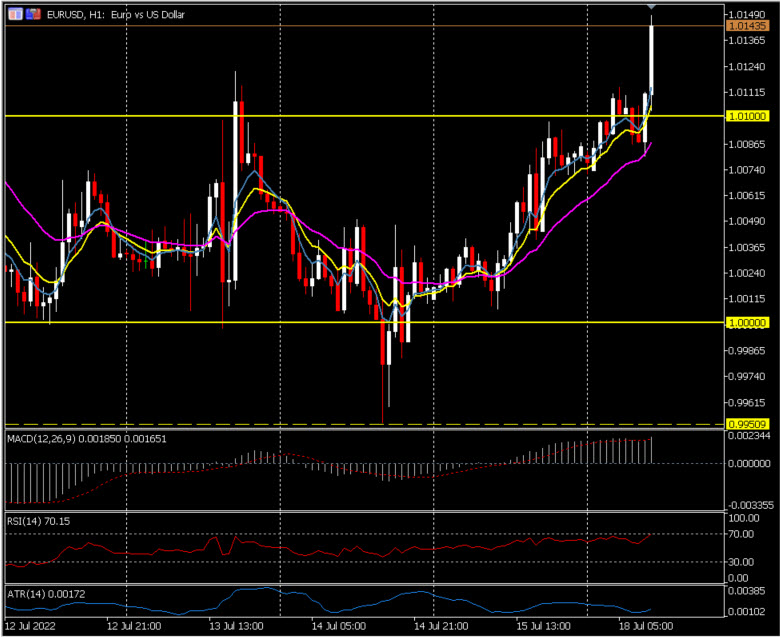

- FX markets – EURUSD hback under 1.0500, USDJPY hit new 24-yr highs at 136.71 and Cable trades down to 1.2225 now, following Inflation news, from 1.2325 highs yesterday.

Today – Canadian CPI, EZ Consumer Confidence, Speeches from Fed’s Powell, Barkin, Evans & Harker, SNB’s Jordan ECB’s de Guindos & Elderson, BoC’s Rogers.

Biggest FX Mover @ (06:30 GMT) NZDUSD (-1.18%). Collapsed from test of 0.6360 on Monday & Tuesday to 0.6250, as NZD Trade Balance missed significantly. MAs aligning lower, MACD histogram negative turning lower, RSI 21.25, OS but still falling, H1 ATR 0.00124, Daily ATR 0.00850.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Stuart Cowell

Head Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.