Date: 24th June 2024.

How Is Politics Trigger a New Wave of Volatility For The Week Ahead?

The US Dollar has been increasing in value against the Japanese Yen for 7 consecutive days. The US Dollar was the best performing currency of the week, while the Japanese Yen was the worst performing. The Japanese Yen Index fell 1.36% during the previous week and a further 0.13% this morning. The currency pair is witnessing strong buy signals from most indicators but is under psychological pressure as investors fear another Japanese Government currency intervention.

However, even with an intervention, fundamental elements continue to point towards potential Dollar strength. Over the past week investors have turned to the Dollar as a “safe haven” ahead of some political uncertainty. The US will hold their first presidential debate which will grab investors attention. The debate on June 27th, will be the first in-person debate between the two main candidates. In addition to this, the French elections will take place over next weekend and is likely to create volatility across the board, particularly if the outcome is a change in leadership.

In addition to the risk factor, the US Dollar also continues to be supported by economic data. While France, Germany and the UK all failed to beat PMI expectations, the US overachieved. The US Services and Manufacturing PMI beat expectations and also rose from the previous month. The Services PMI rose from 54.8 to 55.1 and Manufacturing from 51.3 to 51.7. The only concern for investors is a possible US interest rate adjustment in September 2024 which according to the CME Group is only 59% priced into the market.

Technical analysis, particularly price action is signalling a renewed long signal if the price rises above 159.80. On a 2-hour chart, the price is of the exchange is trading above the 75-bar SMA and 100-bar EMA signalling buyer strength.

USA100 – Apple Warn The EU, But What Will Be The Outcome For the NASDAQ?

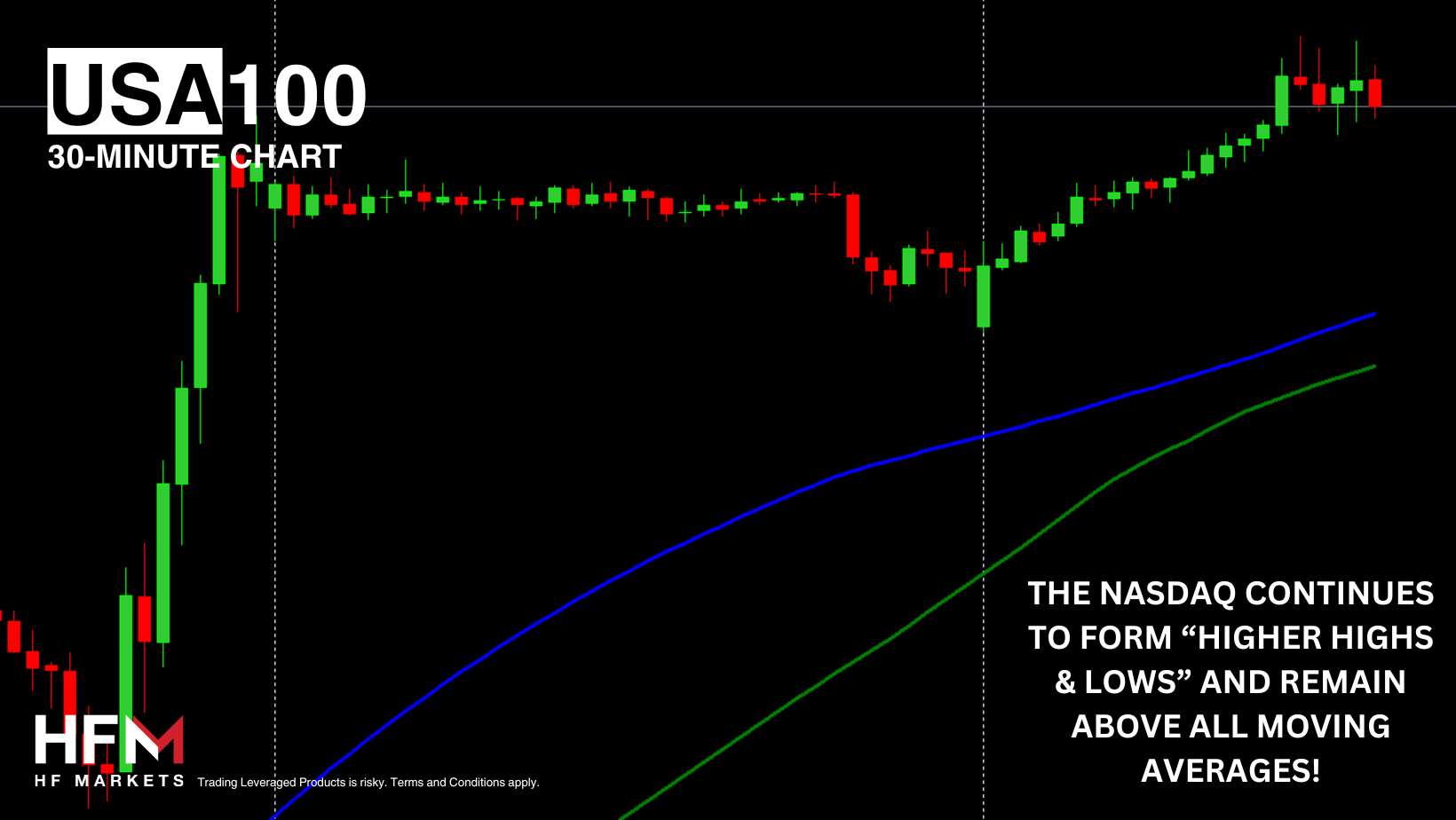

The NASDAQ is trading at the 100-Period EMA for the first time since June 5th as the asset retraces downward. What is pressuring the NASDAQ?

The first catching investors attention is Apple stocks which are the second most influential stock for the index. Apple is warning the EU they will either not release or delay the release of new Apple features within the EU. According to the company, these new features are mainly related to AI which will be released to other regions later in the year.

The DMA is the bloc’s key digital rule book, designed to help local start-ups compete with US-based Big Tech. It requires large digital platforms to share data legally and prohibits them from prioritizing their own services over competitors’. The news is triggering a lack of demand and orders which is causing downward impulse waves.

Another concern for investors is the rise in the US Dollar, the VIX trading 0.70% higher and the lower risk appetite. However, investors will also be keen to see if investors take advantage of the lower price. Analysts continue to believe the longer-term outcome will be a bullish trend as long as market conditions remain strong. A positive aspect for the NASDAQ is that, despite the recent price decline, the High Low Index has rebounded above 60.00%. If the price rises above $19,798.74, a rebound becomes potentially more likely.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Michalis Efthymiou

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

How Is Politics Trigger a New Wave of Volatility For The Week Ahead?

- Apple confirm they will delay the release of certain features within the EU due to regulations.

- Apple stocks fell 3.00% within the past week applying pressure on the NASDAQ.

- The US Dollar was last week’s best performing currency increasing in value by 0.47%.

- Investors turn to haven assets due to political uncertainty. French elections will take place over the weekend and the first US presidential debate on Thursday.

The US Dollar has been increasing in value against the Japanese Yen for 7 consecutive days. The US Dollar was the best performing currency of the week, while the Japanese Yen was the worst performing. The Japanese Yen Index fell 1.36% during the previous week and a further 0.13% this morning. The currency pair is witnessing strong buy signals from most indicators but is under psychological pressure as investors fear another Japanese Government currency intervention.

However, even with an intervention, fundamental elements continue to point towards potential Dollar strength. Over the past week investors have turned to the Dollar as a “safe haven” ahead of some political uncertainty. The US will hold their first presidential debate which will grab investors attention. The debate on June 27th, will be the first in-person debate between the two main candidates. In addition to this, the French elections will take place over next weekend and is likely to create volatility across the board, particularly if the outcome is a change in leadership.

In addition to the risk factor, the US Dollar also continues to be supported by economic data. While France, Germany and the UK all failed to beat PMI expectations, the US overachieved. The US Services and Manufacturing PMI beat expectations and also rose from the previous month. The Services PMI rose from 54.8 to 55.1 and Manufacturing from 51.3 to 51.7. The only concern for investors is a possible US interest rate adjustment in September 2024 which according to the CME Group is only 59% priced into the market.

Technical analysis, particularly price action is signalling a renewed long signal if the price rises above 159.80. On a 2-hour chart, the price is of the exchange is trading above the 75-bar SMA and 100-bar EMA signalling buyer strength.

USA100 – Apple Warn The EU, But What Will Be The Outcome For the NASDAQ?

The NASDAQ is trading at the 100-Period EMA for the first time since June 5th as the asset retraces downward. What is pressuring the NASDAQ?

The first catching investors attention is Apple stocks which are the second most influential stock for the index. Apple is warning the EU they will either not release or delay the release of new Apple features within the EU. According to the company, these new features are mainly related to AI which will be released to other regions later in the year.

The DMA is the bloc’s key digital rule book, designed to help local start-ups compete with US-based Big Tech. It requires large digital platforms to share data legally and prohibits them from prioritizing their own services over competitors’. The news is triggering a lack of demand and orders which is causing downward impulse waves.

Another concern for investors is the rise in the US Dollar, the VIX trading 0.70% higher and the lower risk appetite. However, investors will also be keen to see if investors take advantage of the lower price. Analysts continue to believe the longer-term outcome will be a bullish trend as long as market conditions remain strong. A positive aspect for the NASDAQ is that, despite the recent price decline, the High Low Index has rebounded above 60.00%. If the price rises above $19,798.74, a rebound becomes potentially more likely.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Michalis Efthymiou

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.