Date: 25th July 2024.

Market News – AI mania over? Stocks, Gold & oil dip; Yen Surges.

Economic Indicators & Central Banks:

Financial Markets Performance:

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

------------------------------------------------------------------------------------------------------------------------------------------------

Date: 26th July 2024.

The Yen Soars as the Likelihood of a BoJ Rate Hike Rises!

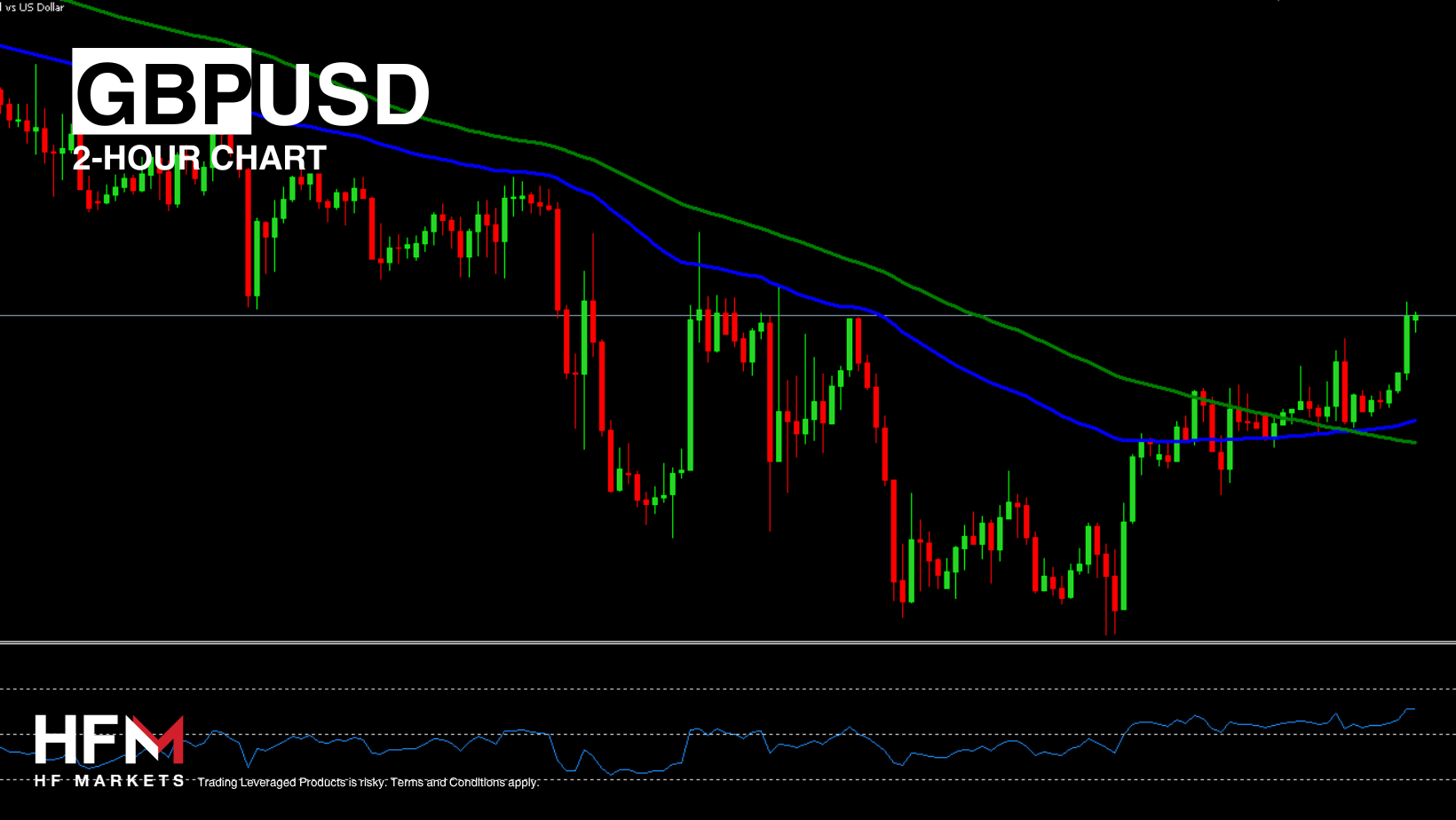

The USDJPY increases in value for a third consecutive week and for a fourth consecutive day. Three factors are contributing to the Dollar decline: The Fed’s upcoming interest cut, the Bank of Japan’s interest rate hike and the political uncertainty in the US. The day’s best performing currency is the Japanese Yen which is currently increasing in value against all currencies.

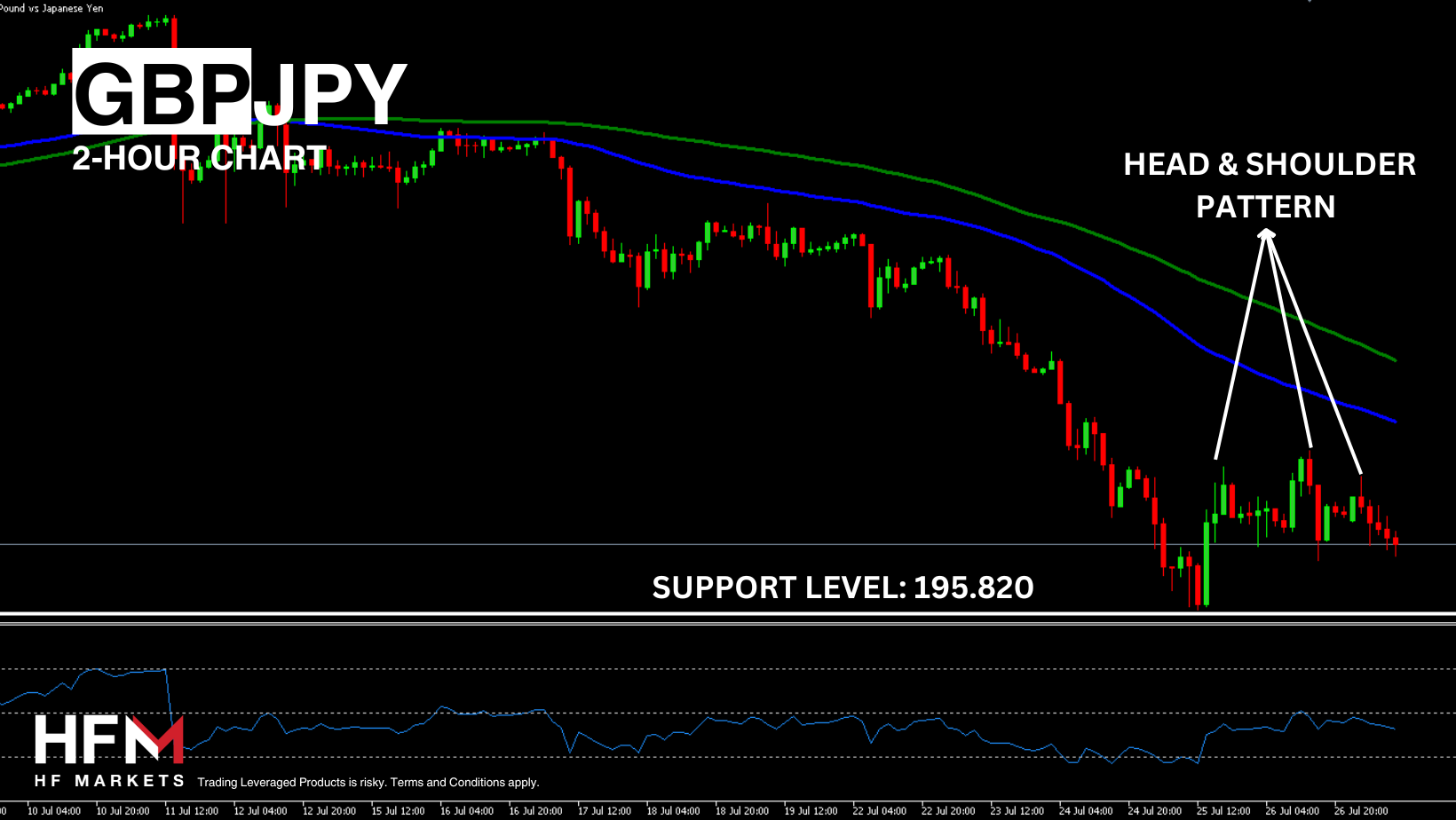

Currently, the USDJPY is trading below the trend-line and below the 100-Period SMA which indicates in the medium-term sellers are controlling the price actions. The exchange rate is also below the neutral on all oscillators and forms a clear bearish trend price pattern. Currently the only indications pointing towards a loss of bearish momentum is the diversion formed on the RSI. As a result, even though the trend clearly forms downwards, investors need to be cautious of a potential retracement. If the price trades above 152.96, a larger retracement becomes likely. However, if the price falls below 152.015, momentum will indicate the continuation of the downward trend to 151.674 in the short term and 151.267 thereafter.

The likelihood of further monetary policy tightening by the Japanese regulator is growing. Preliminary data for July showed an increase in business activity, indicating a recovery in the national economy. The consumer price index remains above the target level, reaching 2.8% in June, with the core indicator stabilizing around 2.6%. Officials are optimistic about maintaining these high levels, supported by significant wage increases.

According to Reuters, Bank of Japan officials will discuss the possibility of raising the interest rate at their meeting on July 31st. Analysts do not expect active measures until after the summer months. However, investors will price in the adjustment before the decision takes place.

The US Fed experts may turn to “dovish” rhetoric in September, which puts pressure on the dollar. Currently, inflation is slowing growth, business activity is declining, and the labor market is showing signs of cooling.

The US PMI data from yesterday largely triggered an attempted bullish correction but was viewed as mixed. The price action of the US Dollar and the USDJPY will now largely depend on the Gross Domestic Product and Weekly Unemployment Claims. These will be made public at 12:30 GMT. Analysts expect the US economy to grow 2.0%. If the US GDP reading is lower than expectations, the US Dollar potentially can come under pressure. At the same time, weaker earnings data from the US can trigger higher demand for the Japanese Yen. The Yen is known as a safe haven currency alternative to the Dollar.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Michalis Efthymiou

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market News – AI mania over? Stocks, Gold & oil dip; Yen Surges.

Economic Indicators & Central Banks:

- Wall Street plunged and Treasuries bear steepened in an anxious trade.

- News that ex-Fed president Dudley was now calling for the FOMC to cut rates next week amid recession fears added to investor angst.

- European stock markets continued to decline alongside Asian equity futures, intensifying a global downturn in technology shares following US session, as investors are pulling back on the artificial-intelligence frenzy that has powered the bull market this year.

- Traders moved away from megacaps to underperforming segments of the market, driven by expectations of Fed rate cuts and doubts about AI’s immediate payoff.

- Nasdaq experienced its largest single-day drop since 2022, while S&P 500 breaks Its longest run without a 2% drop since 2007.

- The Canadian Dollar dropped as the Bank of Canada cut rates, emphasizing “downside risks are taking on increased weight in our monetary policy deliberations.”

- The Japanese Yen reached its highest level since May as carry trades unwound.

- Key events today: Germany IFO business climate, US GDP, initial jobless claims, durable goods.

- Tech led the slump with the NASDAQ dropping -3.64%, the biggest 1-day selloff since March 2020. The S&P500 fell -2.31%. The Dow dropped -1.25%. Disappointing news from Alphabet and Tesla after the bell Tuesday got the bears going and rising concerns over the staying power of AI trades exacerbated declines through the day.

- In Japan, Nikkei entered a technical correction while the broad Topix index, which had reached a record high earlier this month, plunged over 2.5%, erasing its July gains and hitting a five-week low.

- Earning: Apple, Microsoft, Amazon, and Meta are set to report results next week.

Financial Markets Performance:

- The USDIndex tumbled to 104.12 in morning action, down from Tuesday’s 104.45, but rallied back slightly to close at 104.37.

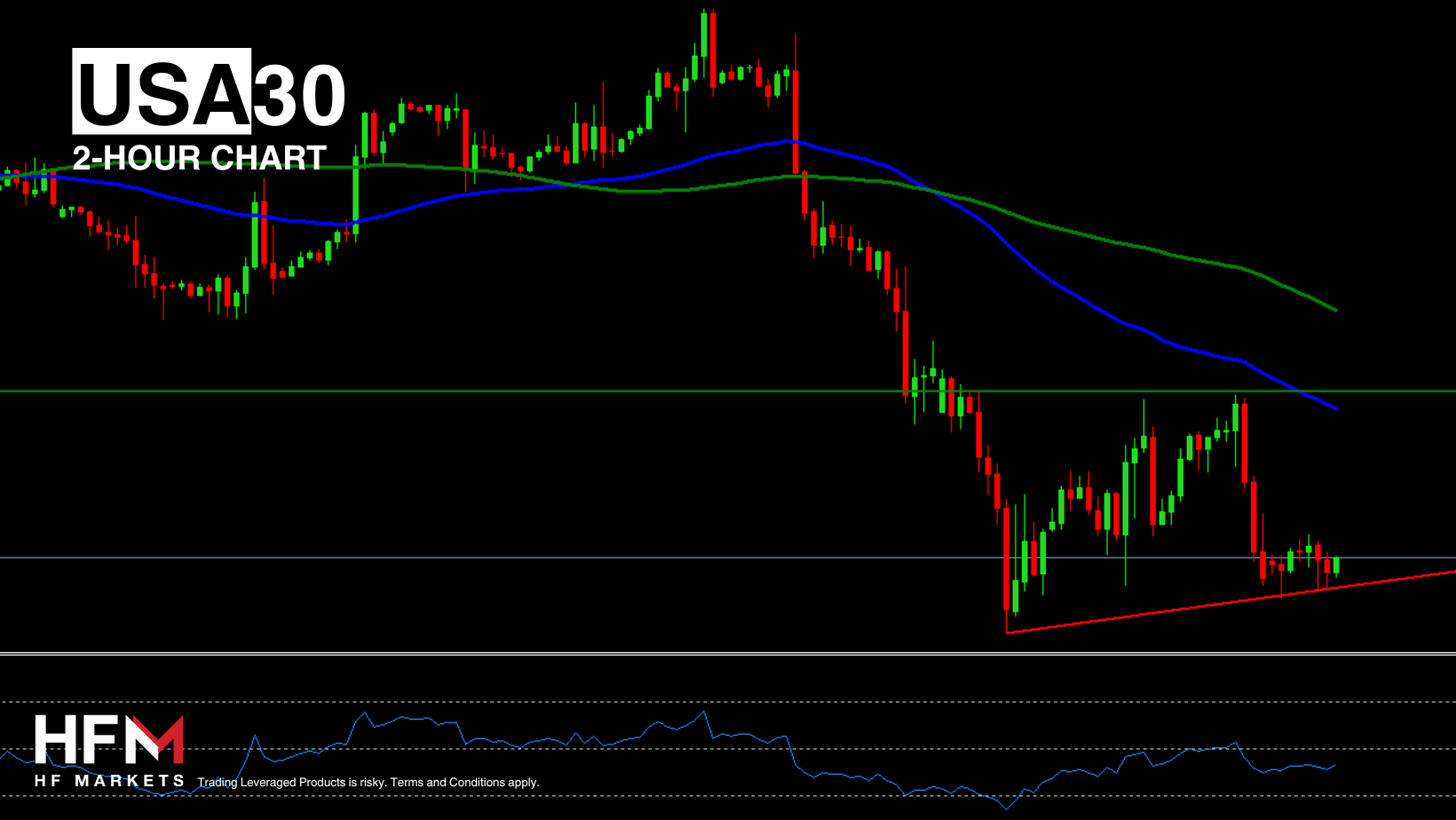

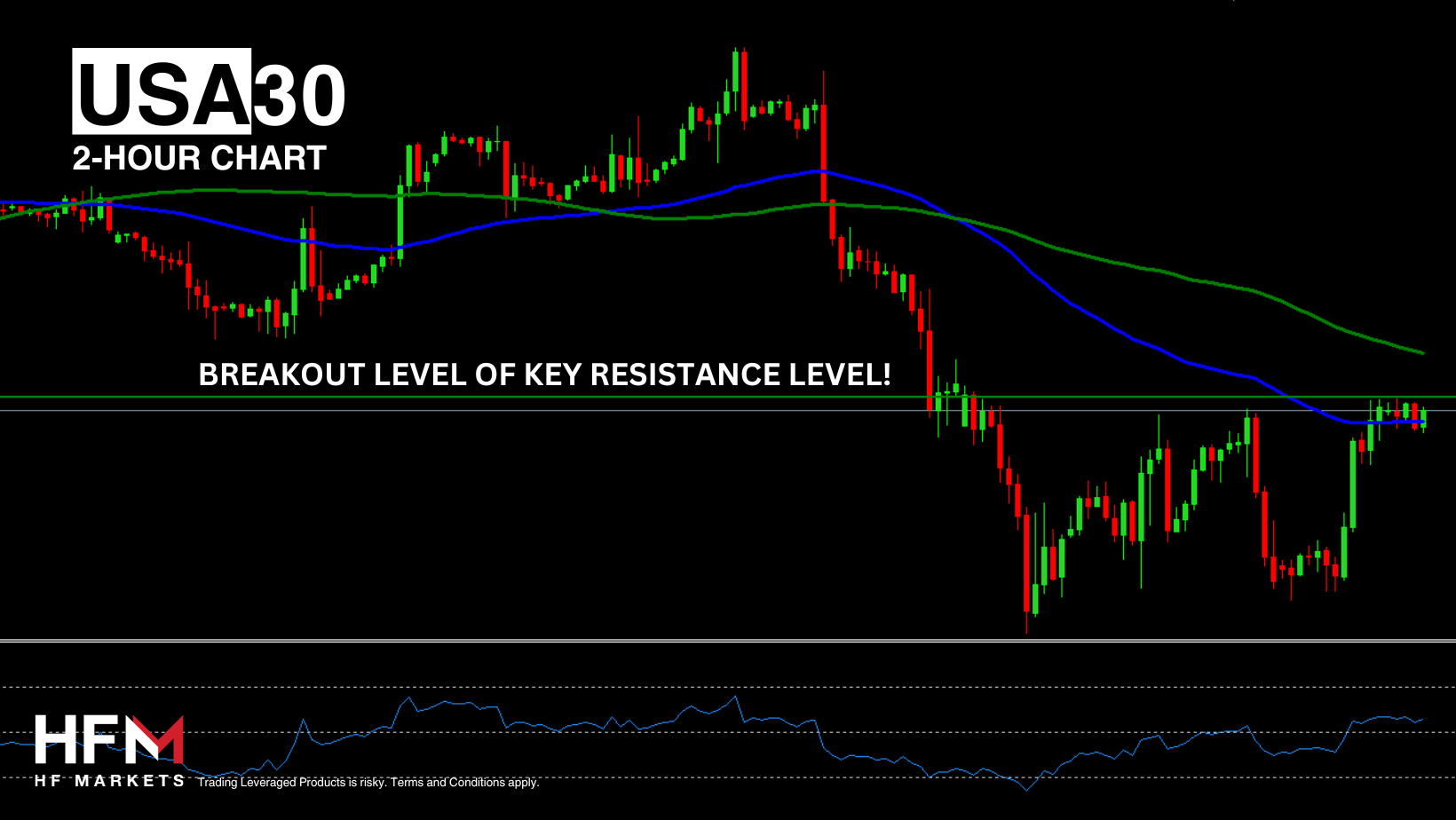

- The Yen holds strong thanks to expectations for a BoJ rate hike next Wednesday, with USDJPY breaching 200-day EMA. The USD firmed versus CAD after the BoC’s dovish cut. The USDCAD reached April’s peak at 1.3827.

- Oil prices declined, but are once again trying to stabilize, following API data showing that US crude inventories declined by 3.9 million barrels last week. Inventories have declined for four straight weeks now. However, weak growth in top importer China and renewed optimism of a ceasefire in the Middle East have kept supply expectations underpinned. WTI is currently trading at USD 77.38 per barrel, Brent at USD 81.49 as markets wait for the official U.S. inventory report.

- Gold is down to $2370 to a two-week low. The downfall could be attributed to some technical selling, though it is expected to be limited, considering the fundamentals, such as Fed’s cut and the risk-off mood which could support Gold ahead of the US data.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

------------------------------------------------------------------------------------------------------------------------------------------------

Date: 26th July 2024.

The Yen Soars as the Likelihood of a BoJ Rate Hike Rises!

- The Japanese Yen wins back some lost ground as global Central Banks edge closer to rate cuts.

- The probability of another interest rate hike by the Bank of Japan increases.

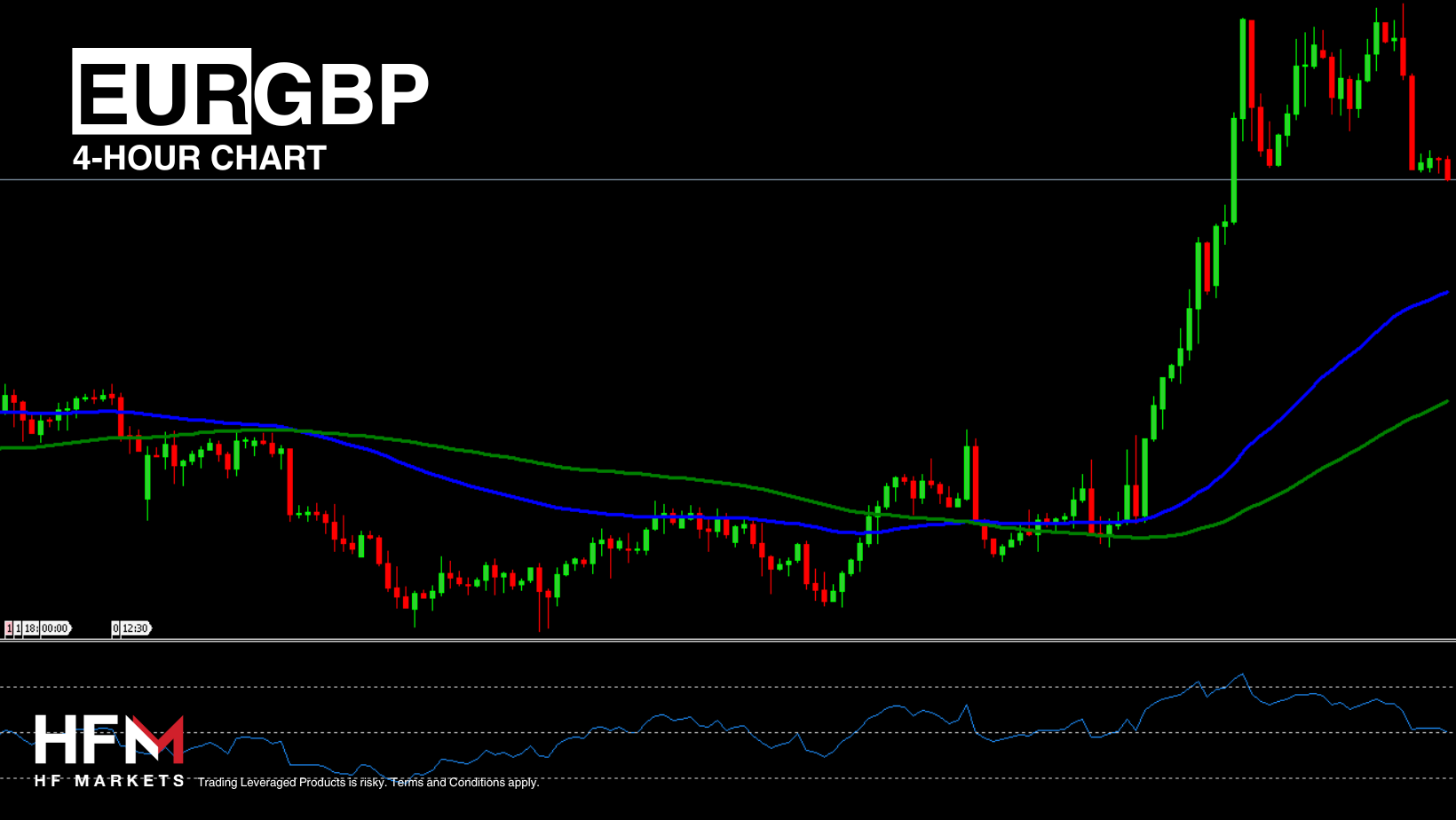

- July’s best performing currencies are the Japanese Yen (+4.35%), British Pound (+1.41%) and the Swiss Franc (+1.41%).

- Currencies are taking advantage of the weaker US Dollar, but the worst performing currency remains the New Zealand Dollar.

The USDJPY increases in value for a third consecutive week and for a fourth consecutive day. Three factors are contributing to the Dollar decline: The Fed’s upcoming interest cut, the Bank of Japan’s interest rate hike and the political uncertainty in the US. The day’s best performing currency is the Japanese Yen which is currently increasing in value against all currencies.

Currently, the USDJPY is trading below the trend-line and below the 100-Period SMA which indicates in the medium-term sellers are controlling the price actions. The exchange rate is also below the neutral on all oscillators and forms a clear bearish trend price pattern. Currently the only indications pointing towards a loss of bearish momentum is the diversion formed on the RSI. As a result, even though the trend clearly forms downwards, investors need to be cautious of a potential retracement. If the price trades above 152.96, a larger retracement becomes likely. However, if the price falls below 152.015, momentum will indicate the continuation of the downward trend to 151.674 in the short term and 151.267 thereafter.

The likelihood of further monetary policy tightening by the Japanese regulator is growing. Preliminary data for July showed an increase in business activity, indicating a recovery in the national economy. The consumer price index remains above the target level, reaching 2.8% in June, with the core indicator stabilizing around 2.6%. Officials are optimistic about maintaining these high levels, supported by significant wage increases.

According to Reuters, Bank of Japan officials will discuss the possibility of raising the interest rate at their meeting on July 31st. Analysts do not expect active measures until after the summer months. However, investors will price in the adjustment before the decision takes place.

The US Fed experts may turn to “dovish” rhetoric in September, which puts pressure on the dollar. Currently, inflation is slowing growth, business activity is declining, and the labor market is showing signs of cooling.

The US PMI data from yesterday largely triggered an attempted bullish correction but was viewed as mixed. The price action of the US Dollar and the USDJPY will now largely depend on the Gross Domestic Product and Weekly Unemployment Claims. These will be made public at 12:30 GMT. Analysts expect the US economy to grow 2.0%. If the US GDP reading is lower than expectations, the US Dollar potentially can come under pressure. At the same time, weaker earnings data from the US can trigger higher demand for the Japanese Yen. The Yen is known as a safe haven currency alternative to the Dollar.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Michalis Efthymiou

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.