Date: 18th October 2024.

Global Markets Steady as China’s Economic Data Surprises, Gold Hits New Record.

As the US economy continues to show resilience, traders further reduced their expectations for Federal Reserve rate cuts in the remaining meetings of 2024. Strong US retail sales data for September exceeded forecasts, highlighting sustained consumer spending, which is powering economic growth.

Asia & European Sessions:

Financial Markets Performance:

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Global Markets Steady as China’s Economic Data Surprises, Gold Hits New Record.

As the US economy continues to show resilience, traders further reduced their expectations for Federal Reserve rate cuts in the remaining meetings of 2024. Strong US retail sales data for September exceeded forecasts, highlighting sustained consumer spending, which is powering economic growth.

Asia & European Sessions:

- A rally in risk and some unwinding of haven trades hit Treasuries.

- A stronger than expected September retail sales report weighed on Treasuries at it furthered expectations the FOMC will reduce rates at a more moderate pace into year end. And it added to prospects the Fed may only cut one more time this year with the November implied rate at -22 bps and the December contract at -41 bps.

- Asia equities rose earlier today as the central bank introduced new lending programs to boost corporate share buybacks and equity purchases. However Chinese equities edged down after official data showed slowing economic growth at 4.6% in the Q3 from 4.7% in Q2, underscoring investor uncertainty over government stimulus measures first announced in September.

- Netflix reported net income of $2.36 billion, roughly 6% above Wall Street predictions. Netflix saw a stronger-than-anticipated revenue boost in the latest quarter, alongside solid subscriber (5.1mln) growth, even with fewer blockbuster releases.

Financial Markets Performance:

- The USDIndex climbed to 103.60,supported by widening rate and growth differentials. The downshift in expectations on Fed cuts, this week’s easing, albeit cautious, from the ECB, the chance for an aggressive -50 bp easing from the BoC, and the unwinding of BoJ rate hike outlooks have been supportive.

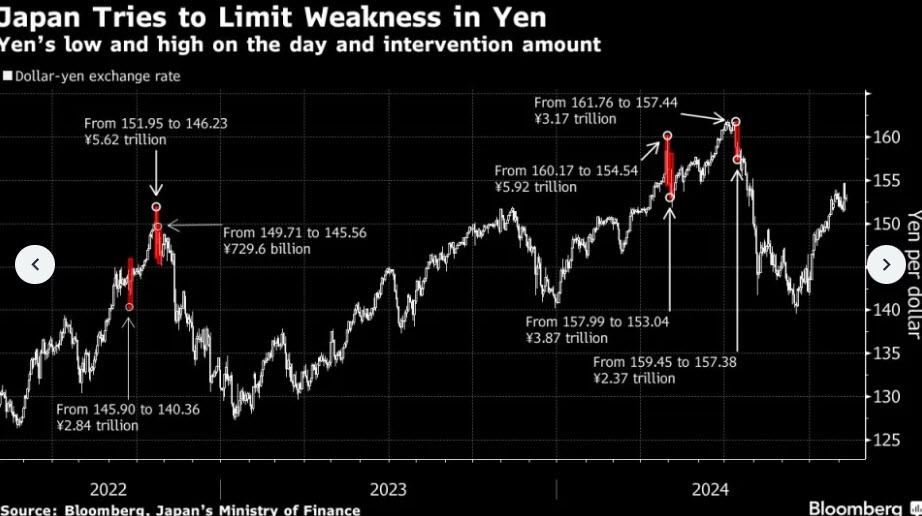

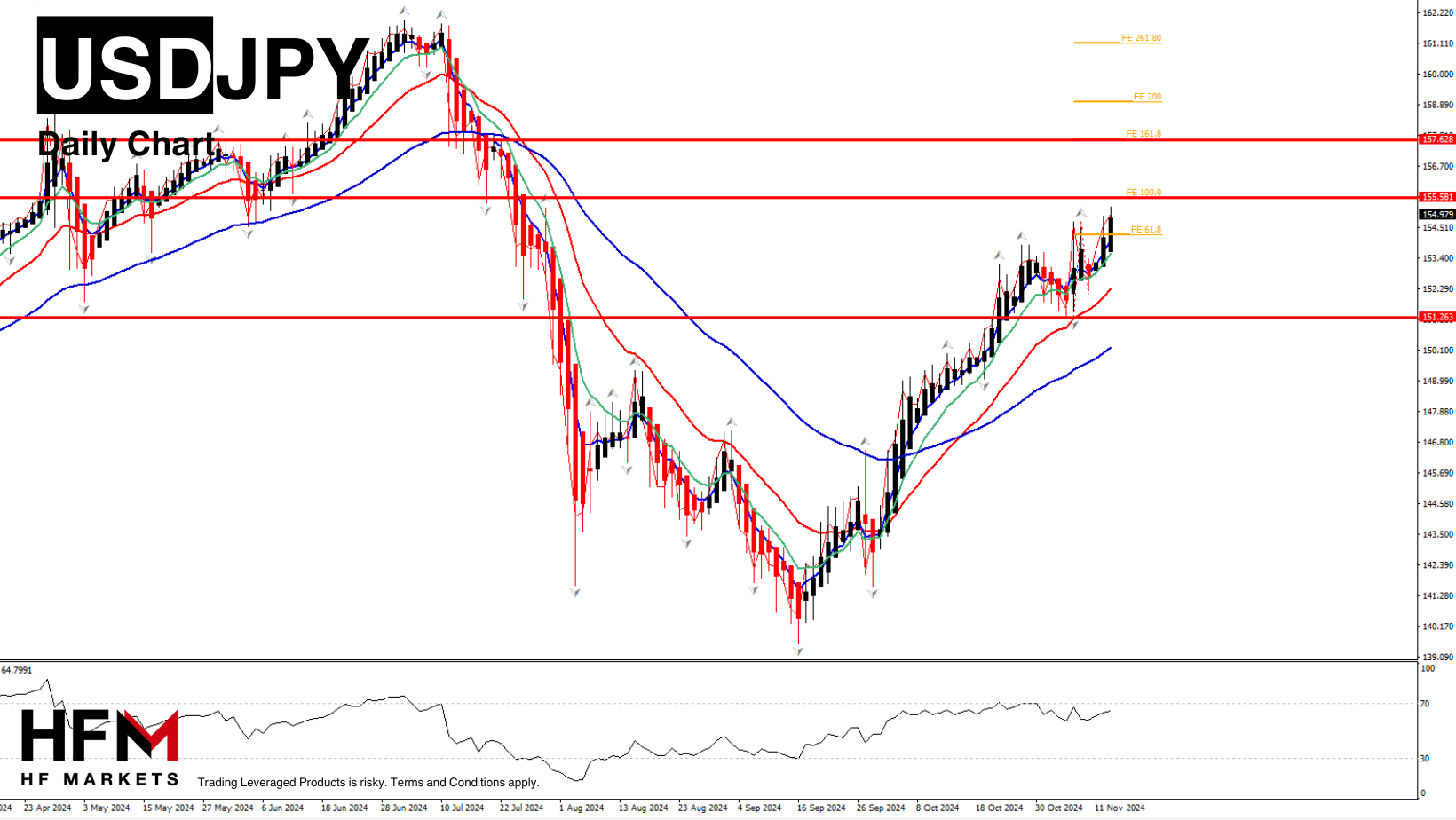

- The USDJPY broke to 150 level, the best since the end of July. It could rally further given the less dovish view on the Fed and if there are no signs of MoF intervention.

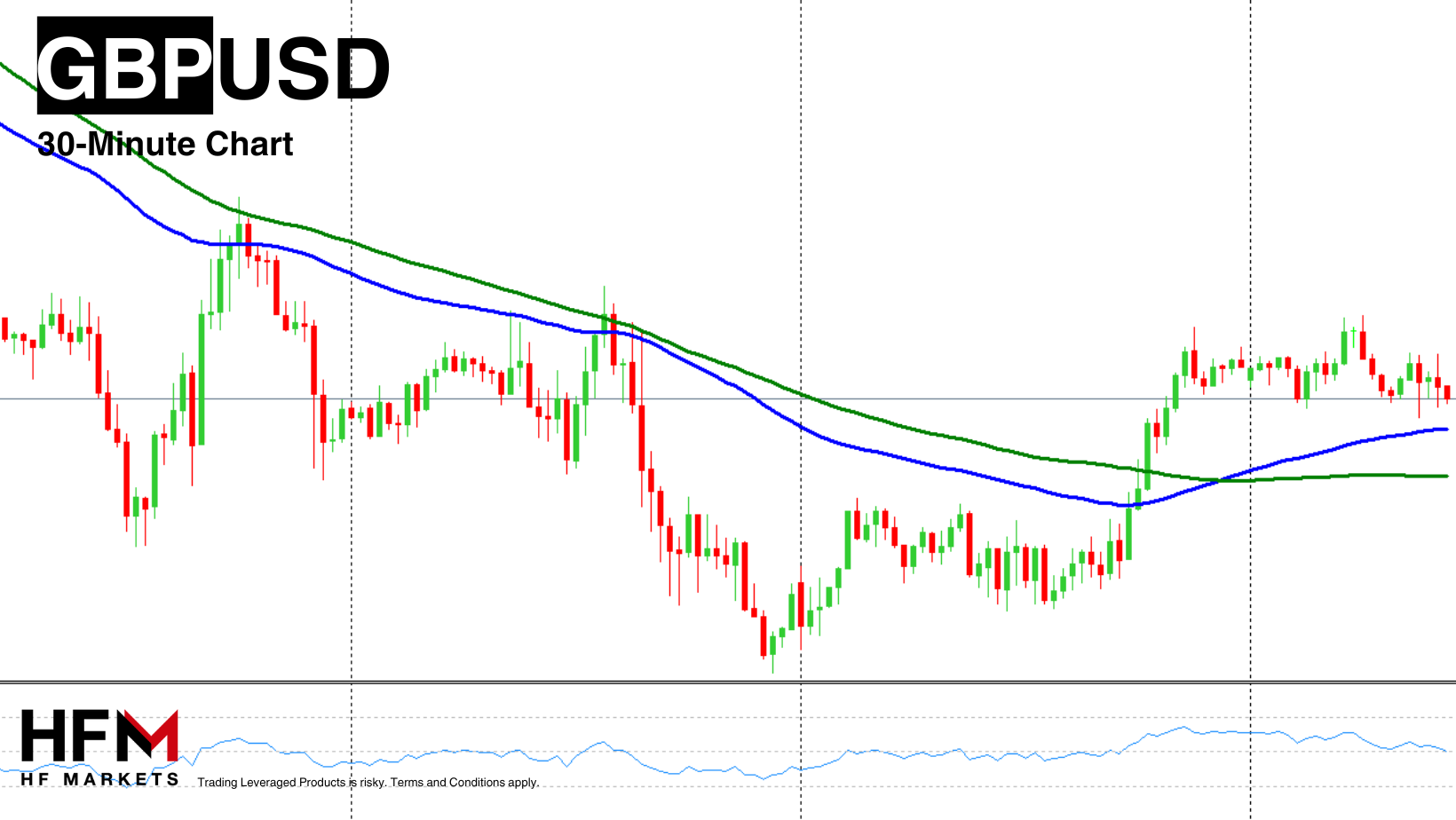

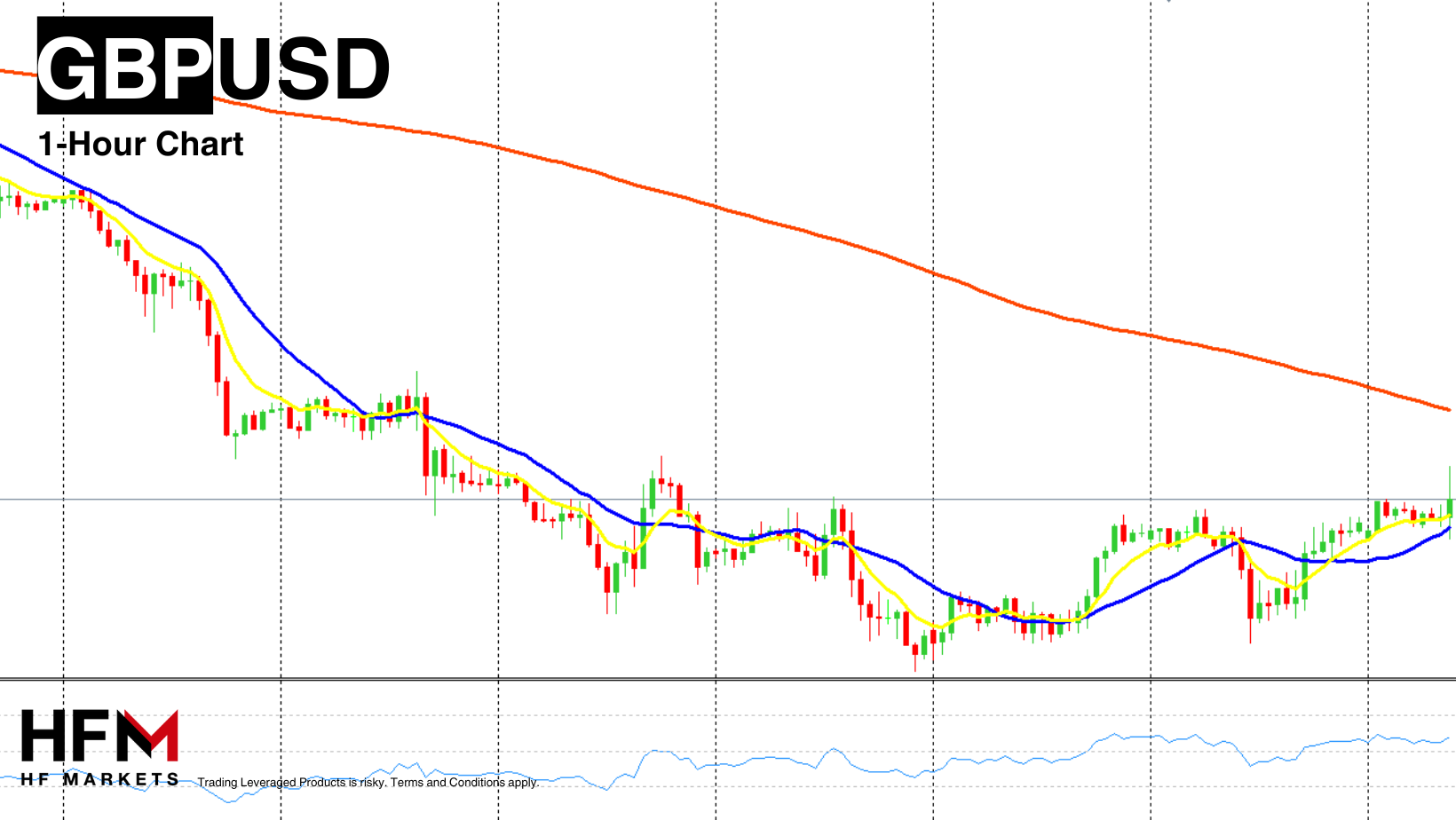

- The GBPUSD has stabilized and firmed slightly to 1.3060, but is largely recovering from the drop to 1.2990 which is the weakest since mid-August.

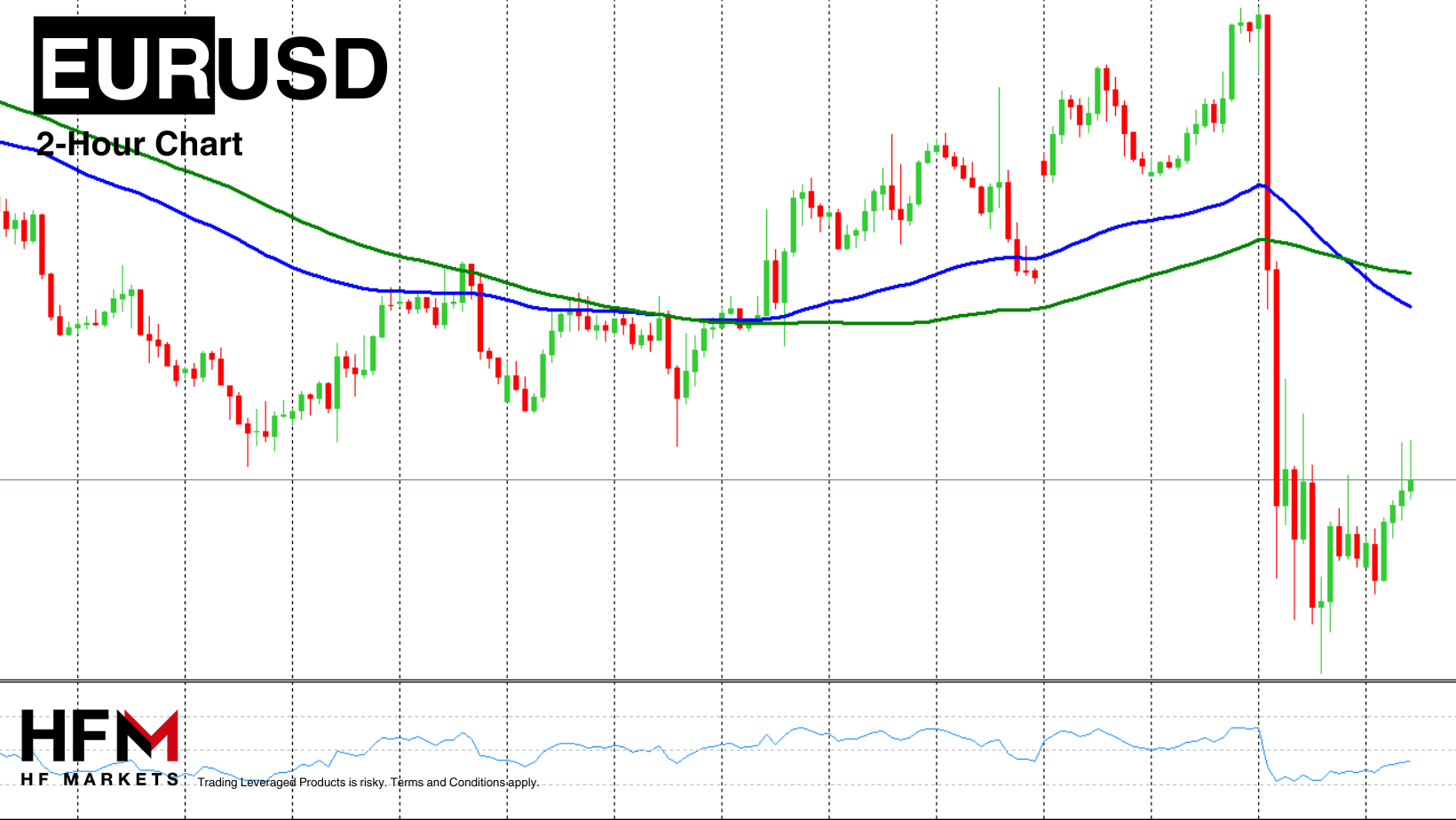

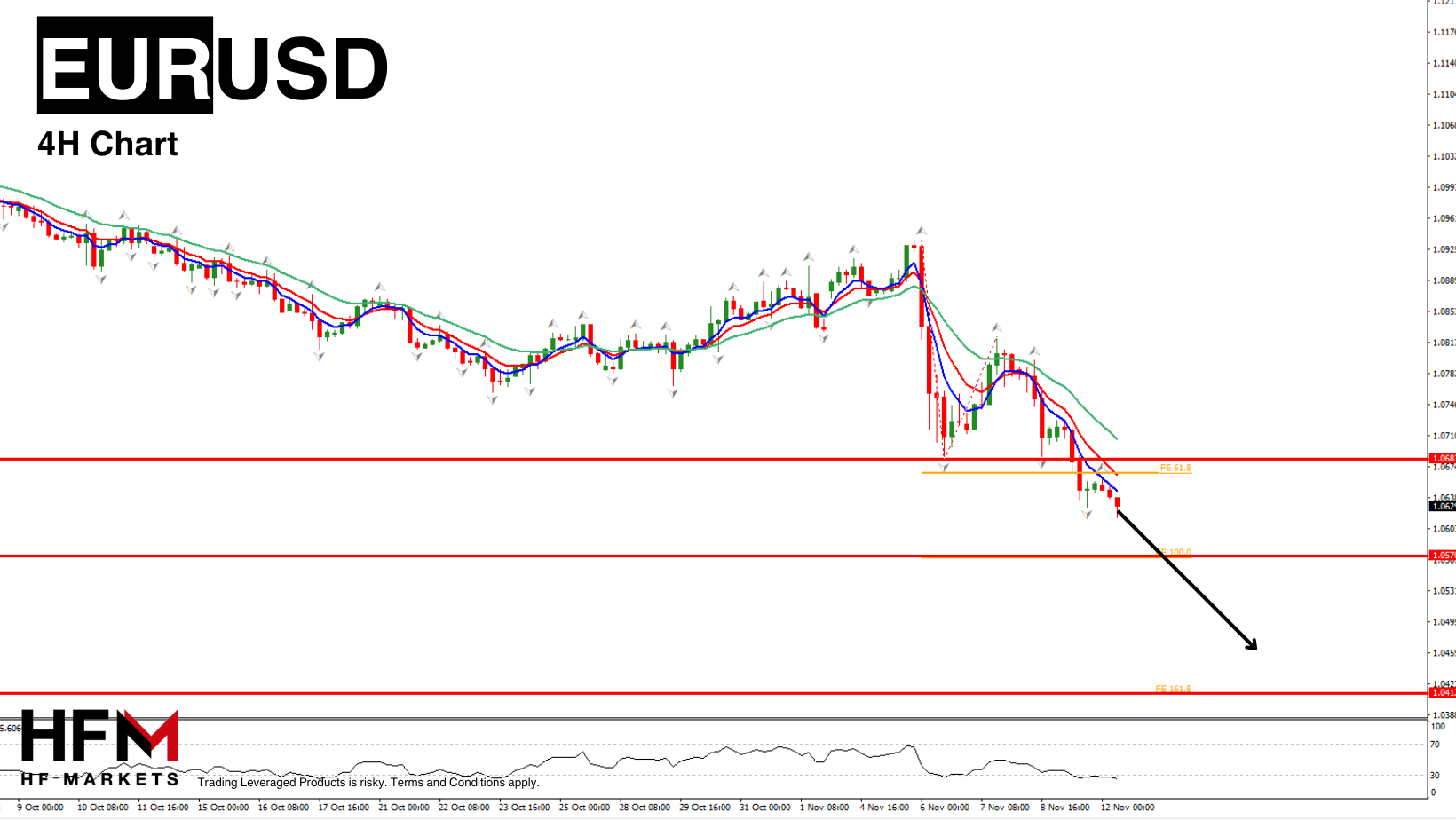

- The EURUSD has slumped to 1.0807 and is the weakest since the end of July. Concurrently, USDCAD has risen to 1.3795, the highest since early August.

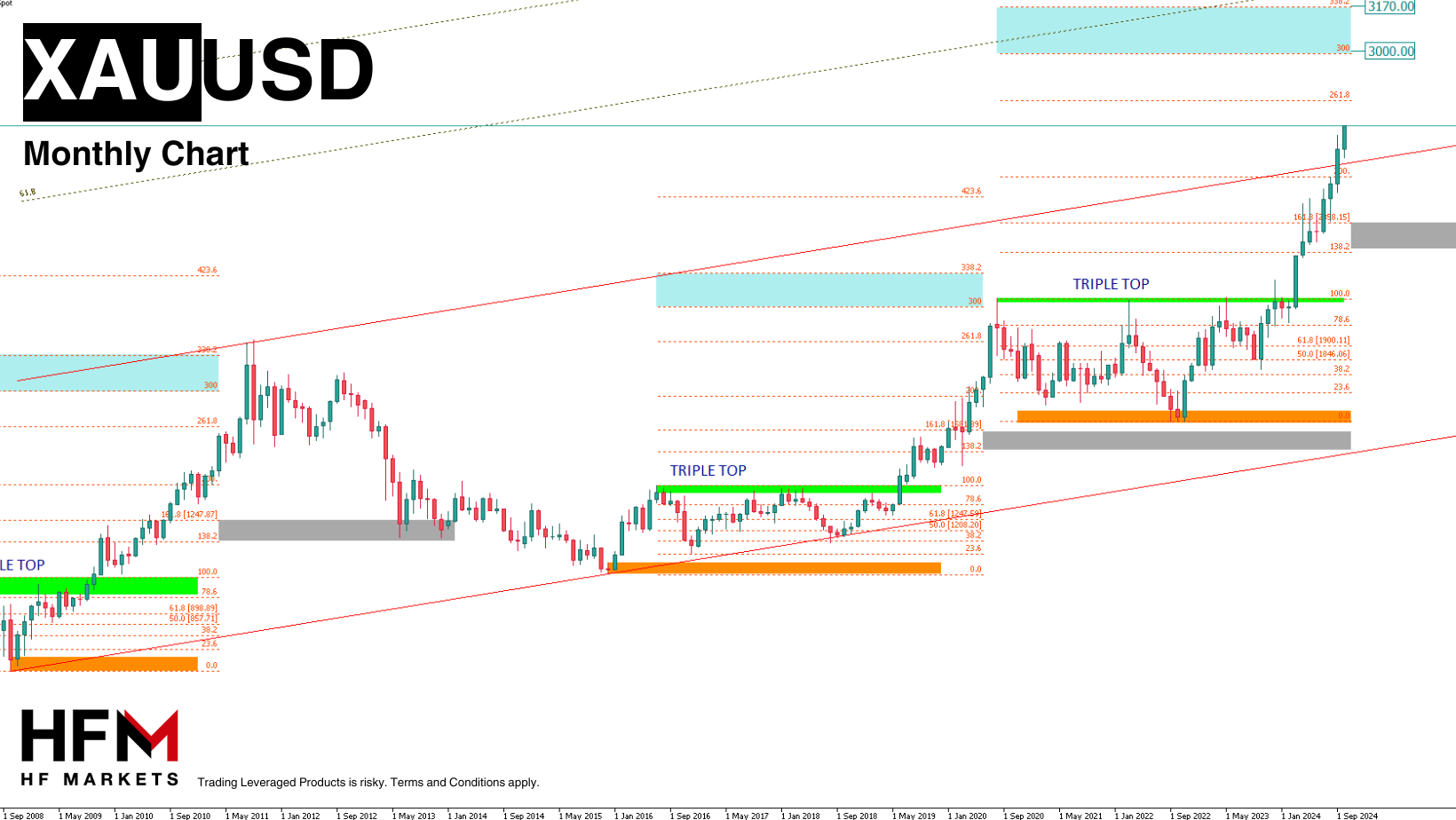

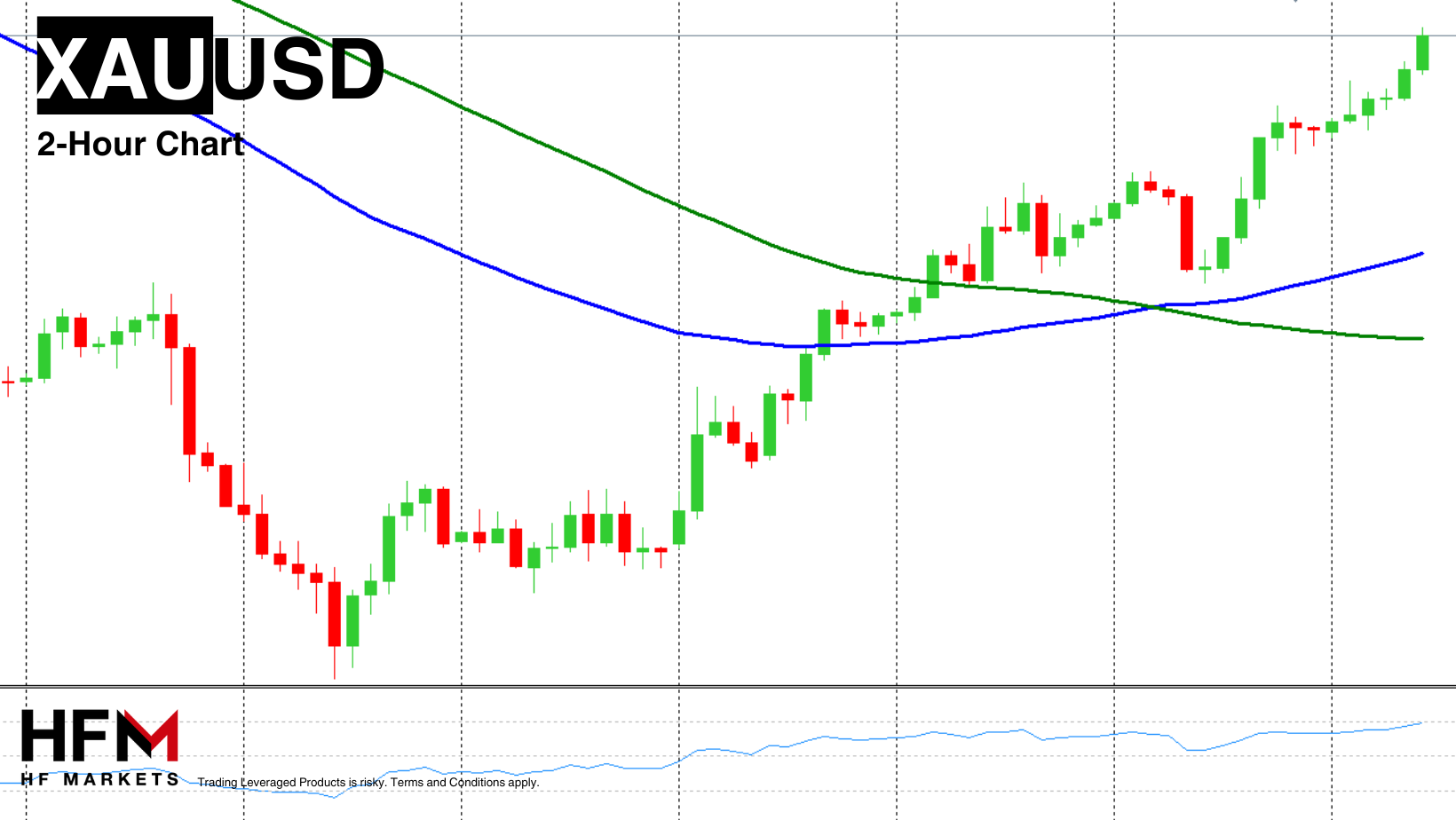

- Gold prices hit a record high, extending a long-running bullish trend as investors sought safe-haven assets. Gold spot prices rose to $2,713. The rise in gold prices, fueled by inflation and geopolitical uncertainty, has been consistent since late 2022.

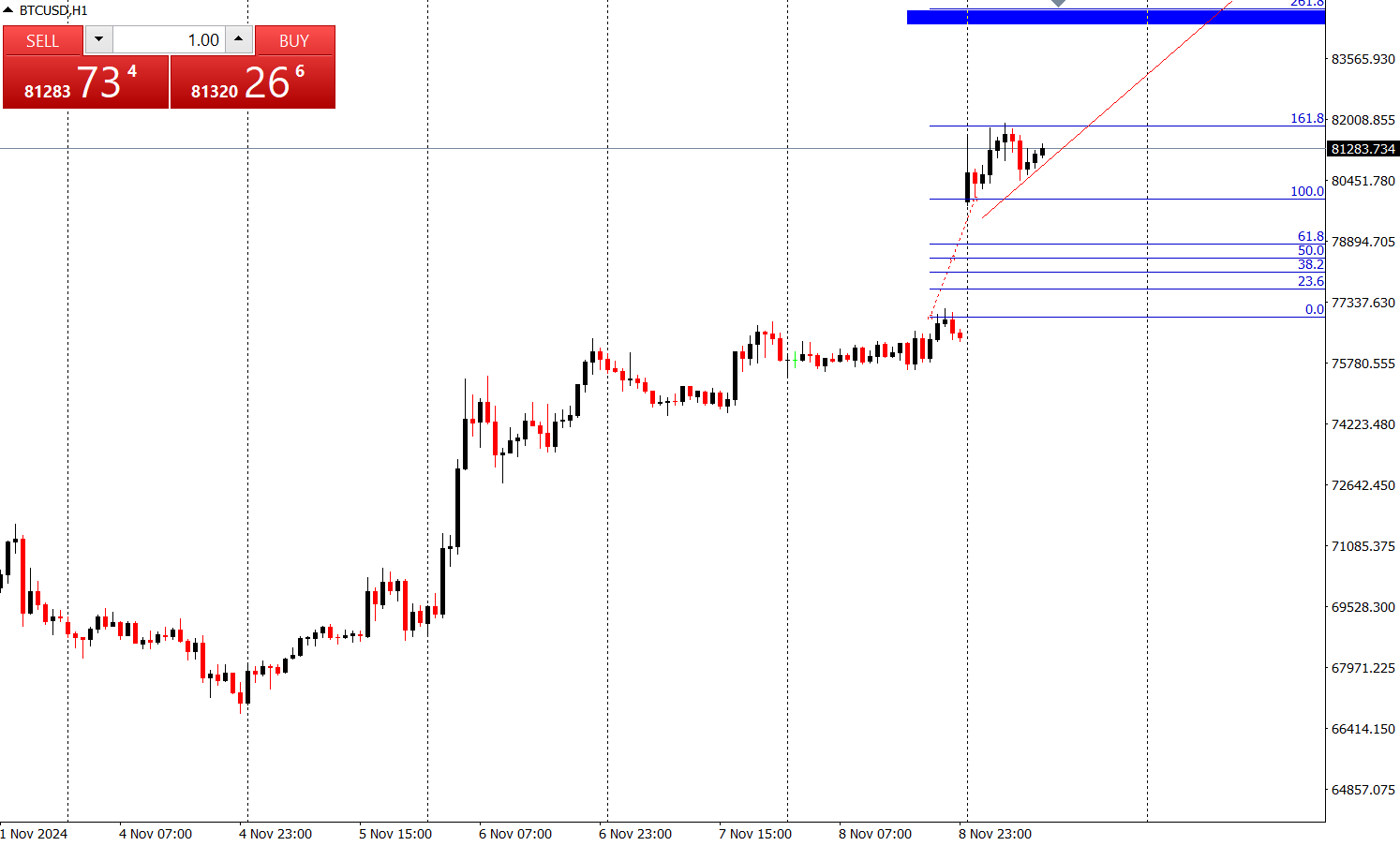

- Bitcoin also saw gains, rising to $68,350, with some investors viewing it as a hedge similar to gold.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.