Date: 4th September 2024.

Stocks Suffer Sharpest Drop Since August 5th, What’s Next?

The NASDAQ is trading at its lowest price since August 13th after witnessing its worst trading day since August 5th. Throughout all 3 trading sessions the price of the index fell 3.40% and is now trading firmly below trend lines and neutral levels on Oscillators. The question now is whether the price is oversold and if investors are unwilling to trade at such high prices.

The decline was not solely related to the NASDAQ, but the whole US stock market as well as global stocks. The NIKKEI225 fell a further 1.50% today and the DAX is due to open 0.60% lower. Simultaneously the VIX is trading higher for a third consecutive day. These are known to be indications of lower sentiment towards stocks.

The decline came about due to the lower risk appetite, the unwinding of hedge positions which involved the Japanese Yen and fear of lower consumer demand. The index was also influenced by the higher PMI data from the ISM which indicated higher economic sentiment. As a result, a 50-basis point rate cut becomes less likely applying further pressure on the stock market. However, this will also depend on this week’s employment data and next week’s inflation rate.

All of the 12 most influential stocks fell in value and of the top 50 influential only 7 ended the day at a higher price. The question now is whether investors will now look to purchase the lower price. This will largely depend on today’s JOLTs Job Openings which analysts expect to read slightly above 8 million. Ideally investors will want to see higher job openings in order to give them confidence the consumer demand will not fall. According to economists, even with a slightly higher figure, the Federal Reserve is still likely to cut interest rates.

Since the opening of the European Cash Open, the VIX has slightly fallen and European stocks are attempting a rebound. This is also something traders will monitor because if the momentum continues it may indicate a different price movement, such as a correction. Nonetheless, this will still largely depend on today’s release.

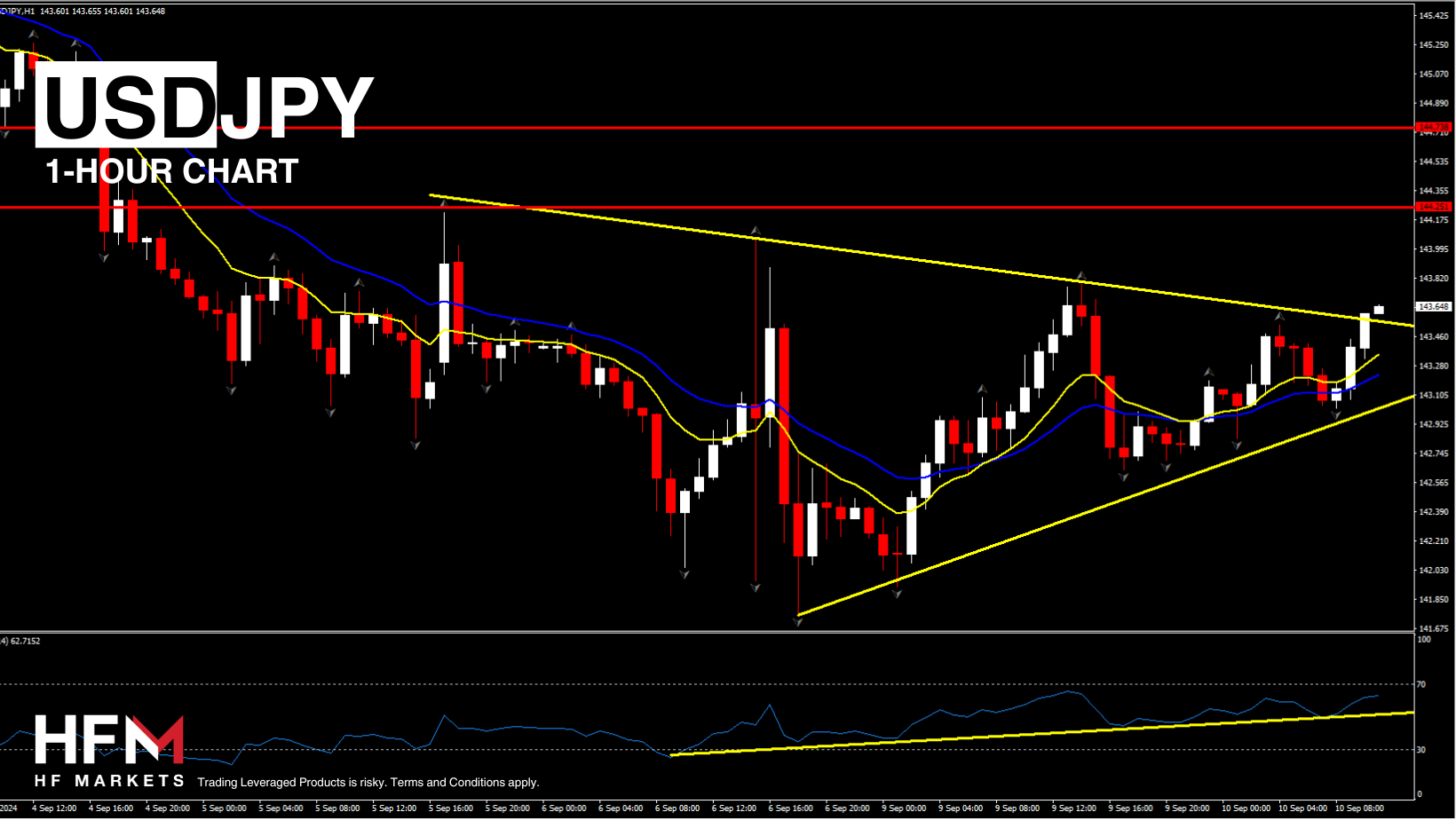

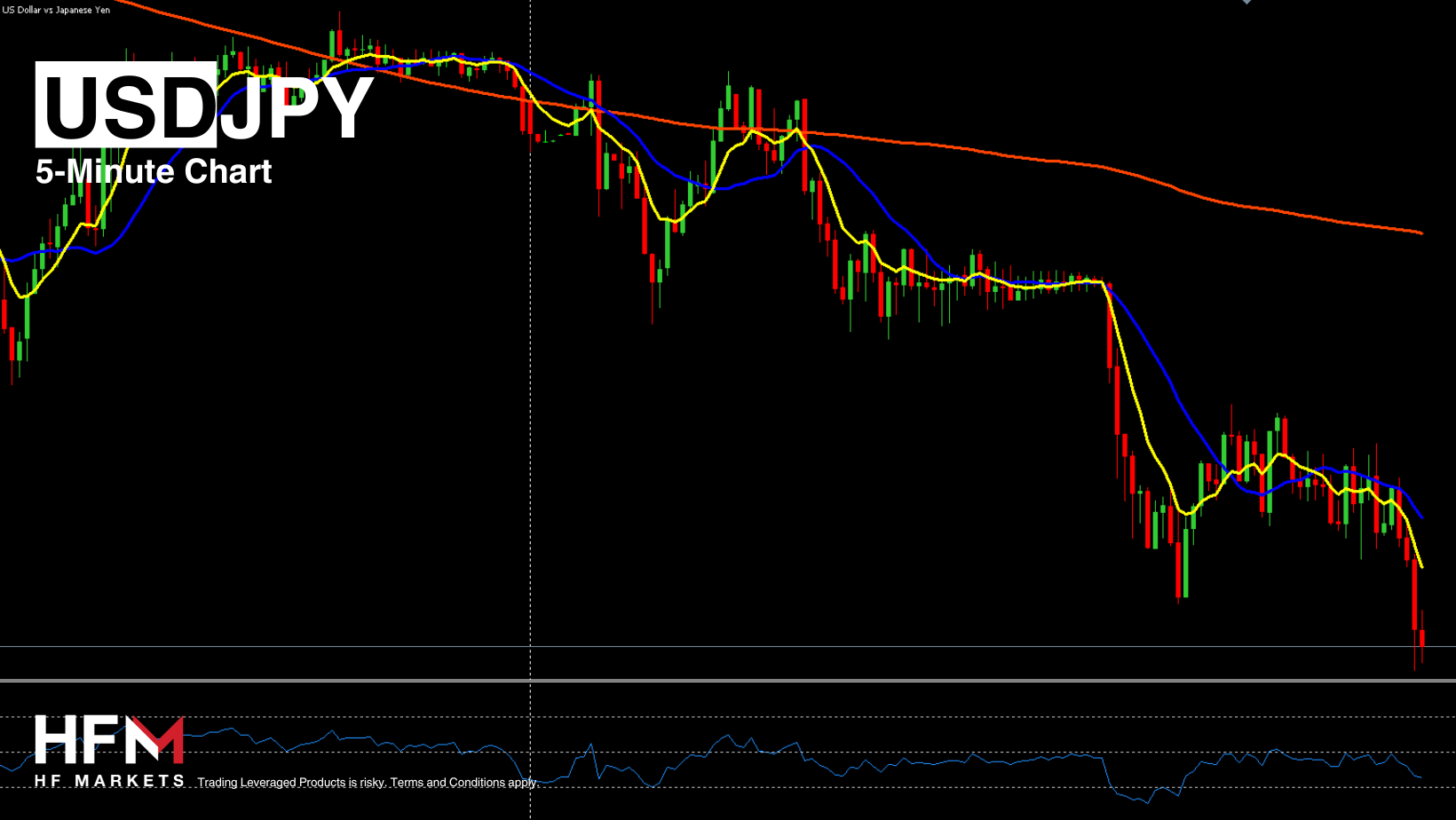

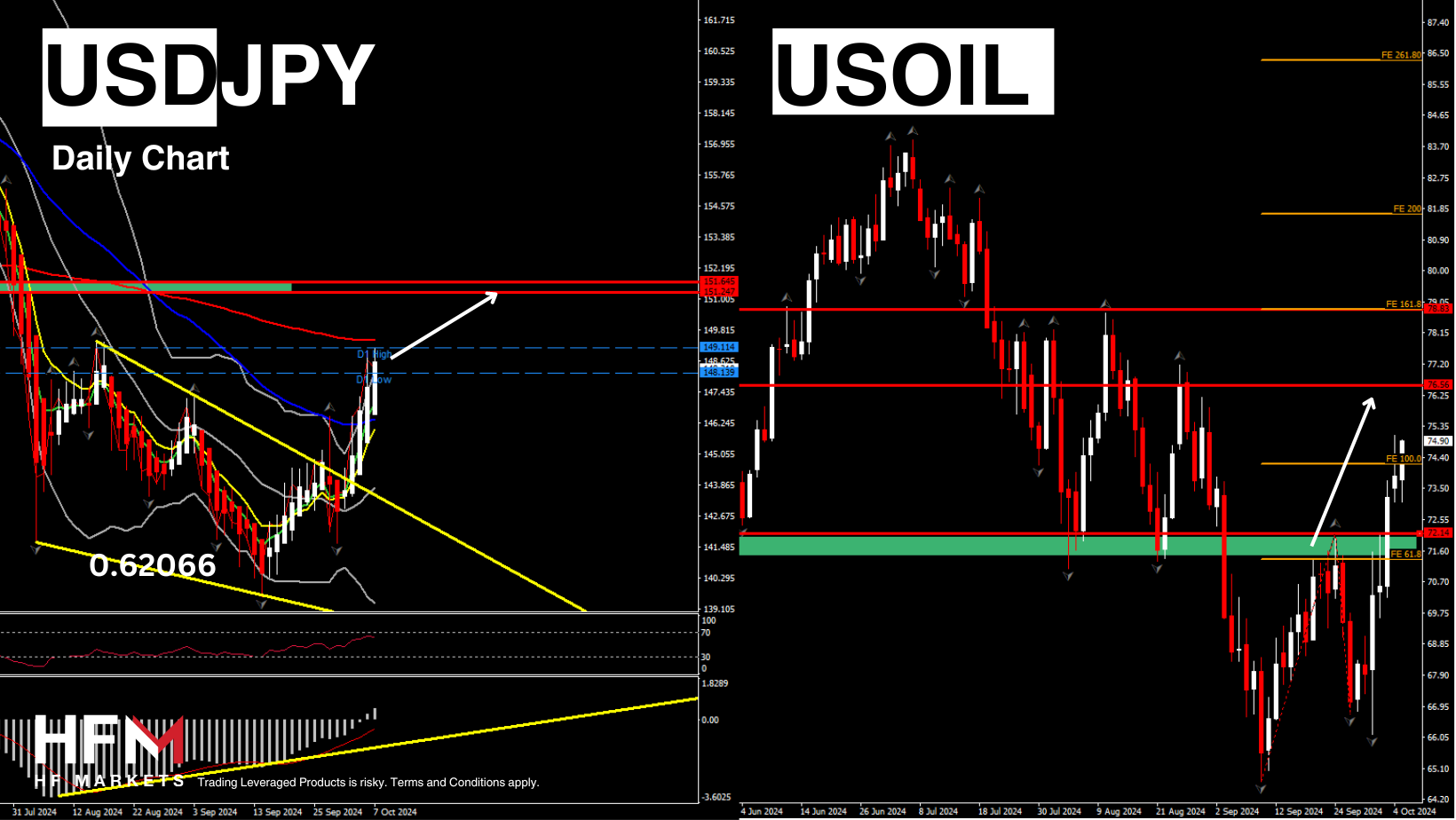

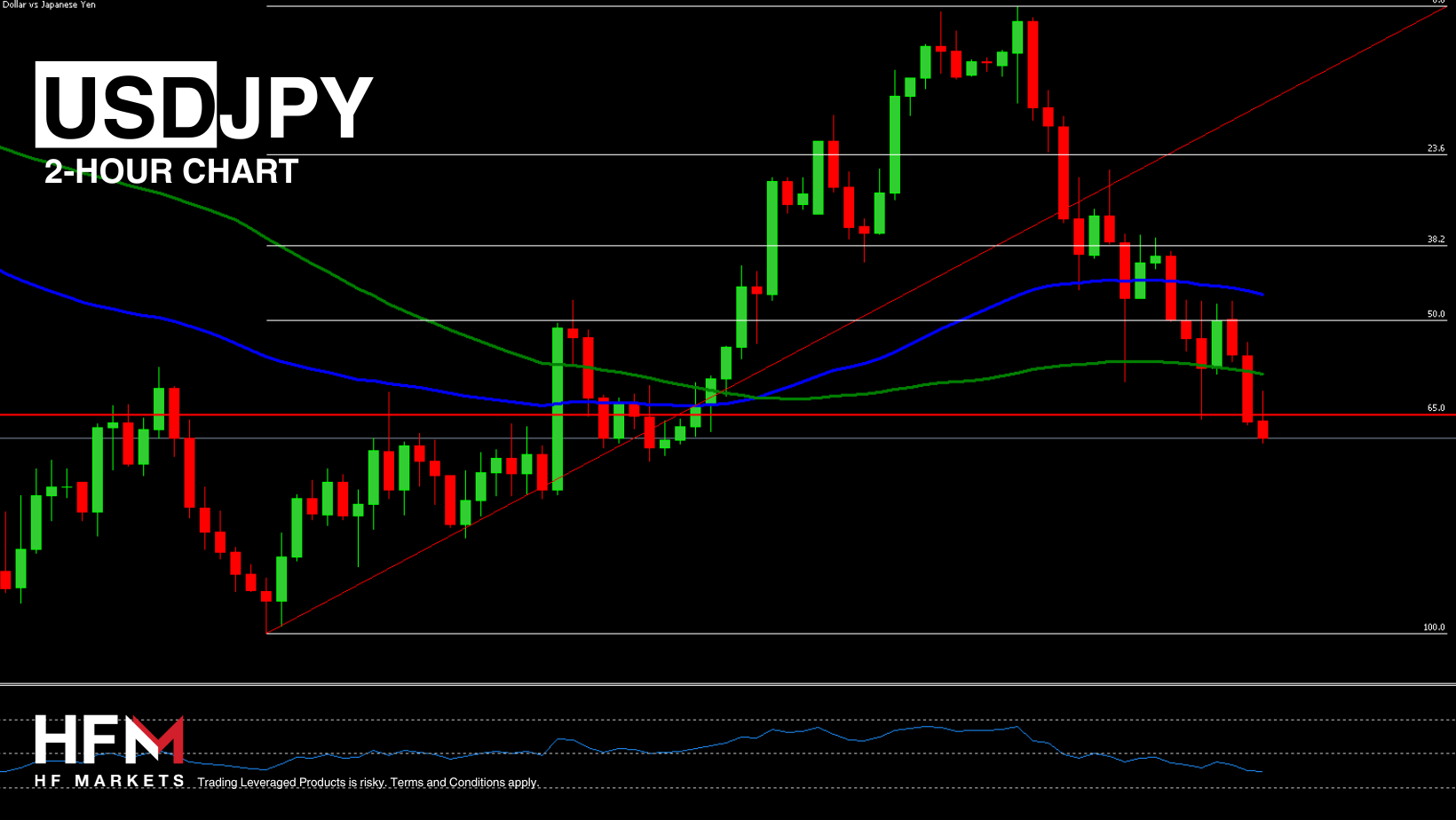

USD/JPY – Technical Analysis

The Japanese Yen is the day’s best performing currency while the US Dollar is the worst performing currency. The USDJPY is also trading below the trend-line, 100-Period SMA and below the 50.00 level on the RSI. The exchange rate has also fallen below 144.904 which is a key level on the Fibonacci levels.

The Institute for Supply Management reported that in August, the US Manufacturing PMI increased slightly from 46.8 to 47.2 points, but still signals a slowdown in the industry. This slowdown meets the Federal Reserve’s conditions for easing monetary policy. Many experts now expect the Fed to lower interest rates three times, by a total of 100 basis points, by the end of the year. If the day’s JOLTS Job Openings read lower than 8 million, the US Dollar can witness higher downward momentum.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Michalis Efthymiou

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Stocks Suffer Sharpest Drop Since August 5th, What’s Next?

- The stock market witnesses its worst session since August 5th. The NASDAQ drops more than 3.00% as 80% of its stocks decline.

- The VIX rises more than 5% indicating a low risk appetite as investors fear lower consumer demand and the unwinding of certain hedge positions.

- The price of the Japanese Yen increases in value for a second consecutive day.

- ISM PMI data improves but investors turn their attention to JOLTS Job Openings and NFP.

The NASDAQ is trading at its lowest price since August 13th after witnessing its worst trading day since August 5th. Throughout all 3 trading sessions the price of the index fell 3.40% and is now trading firmly below trend lines and neutral levels on Oscillators. The question now is whether the price is oversold and if investors are unwilling to trade at such high prices.

The decline was not solely related to the NASDAQ, but the whole US stock market as well as global stocks. The NIKKEI225 fell a further 1.50% today and the DAX is due to open 0.60% lower. Simultaneously the VIX is trading higher for a third consecutive day. These are known to be indications of lower sentiment towards stocks.

The decline came about due to the lower risk appetite, the unwinding of hedge positions which involved the Japanese Yen and fear of lower consumer demand. The index was also influenced by the higher PMI data from the ISM which indicated higher economic sentiment. As a result, a 50-basis point rate cut becomes less likely applying further pressure on the stock market. However, this will also depend on this week’s employment data and next week’s inflation rate.

All of the 12 most influential stocks fell in value and of the top 50 influential only 7 ended the day at a higher price. The question now is whether investors will now look to purchase the lower price. This will largely depend on today’s JOLTs Job Openings which analysts expect to read slightly above 8 million. Ideally investors will want to see higher job openings in order to give them confidence the consumer demand will not fall. According to economists, even with a slightly higher figure, the Federal Reserve is still likely to cut interest rates.

Since the opening of the European Cash Open, the VIX has slightly fallen and European stocks are attempting a rebound. This is also something traders will monitor because if the momentum continues it may indicate a different price movement, such as a correction. Nonetheless, this will still largely depend on today’s release.

USD/JPY – Technical Analysis

The Japanese Yen is the day’s best performing currency while the US Dollar is the worst performing currency. The USDJPY is also trading below the trend-line, 100-Period SMA and below the 50.00 level on the RSI. The exchange rate has also fallen below 144.904 which is a key level on the Fibonacci levels.

The Institute for Supply Management reported that in August, the US Manufacturing PMI increased slightly from 46.8 to 47.2 points, but still signals a slowdown in the industry. This slowdown meets the Federal Reserve’s conditions for easing monetary policy. Many experts now expect the Fed to lower interest rates three times, by a total of 100 basis points, by the end of the year. If the day’s JOLTS Job Openings read lower than 8 million, the US Dollar can witness higher downward momentum.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Michalis Efthymiou

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.